NFI Reactions to the SEC v. Coinbase Opinion

It is the right decision, but is it on the right path?

The long-awaited decision in SEC v. Coinbase is out. For the most part, the case remains intact, and to quote Ripple’s CLO, Steve Alderoty, the crypto industry didn’t achieve the “quick knockout punch” it was hoping for. This particular outcome wasn’t unexpected; motions to dismiss are very tough to win. Jeremy Hogan’s prediction that some parts would fall off and the rest would move to discovery turned out to be fairly accurate. The consensus was that the Court wouldn’t dismiss the parts of the case (indeed it didn’t) that involve the core question: Do crypto purchases on the secondary market constitute investment contracts?

You may recall that we submitted an amicus brief in support of the SEC, urging the Court to deny Coinbase’s Motion to Dismiss. The outcome is in line with the narrative that we were advancing, but the Court reached that outcome via a different path. Our concern is that, in the long run, it makes the decision vulnerable at the expense of the investing public. Here is why:

Framing the Problem

Judge Failla frames the problem as the clash of the following views:

[T]he SEC argues that the absence of post-sale obligations is not dispositive as to the existence of an investment contract, and should not foreclose the securities laws from applying in circumstances where token holders reasonably expect the value of their asset to increase based on the issuer’s broadly-disseminated plan to develop and maintain the asset’s ecosystem.

vs.

Coinbase sharply parts ways with the SEC on the question of whether secondary market transactions can constitute investment contracts. Because an issuer owes no contractual obligation to a retail buyer on the Coinbase Platform or through Prime, Coinbase argues that these transactions in the Crypto-Assets do not constitute “investment contracts,” and are therefore not “securities,” such that Coinbase’s conduct does not fall within the ambit of the securities laws. (internal citations omitted)

The framing is not incorrect, but we don’t believe it’s the most optimal way to frame the issue. Part of the problem is the fact that the SEC hangs its hat on this so-called “ecosystem” concept. That was enough for them to survive at this stage, but will it hold up?

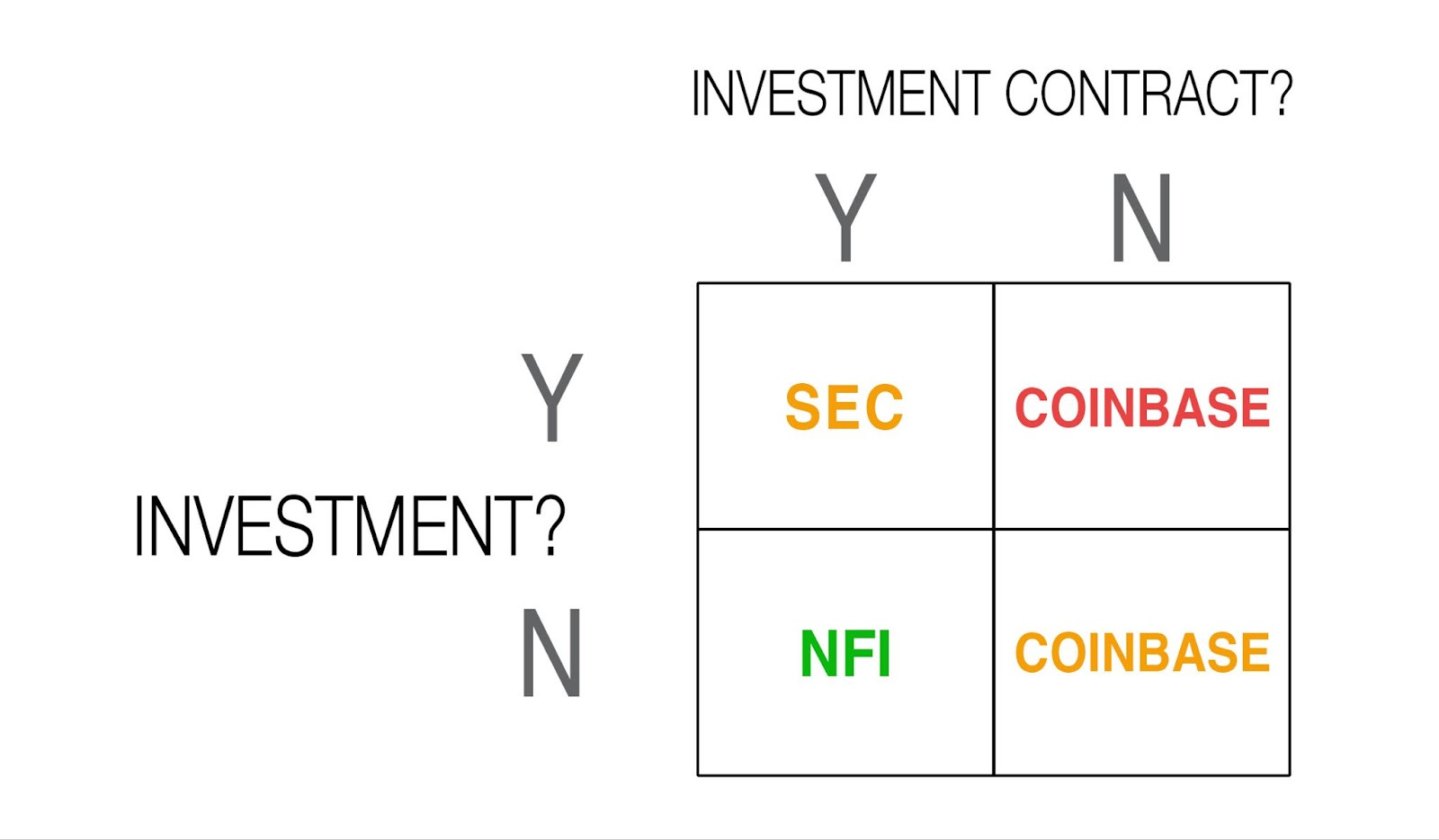

We believe the 2x2 table described in our amicus is a better framing choice. We started talking about this framing back in June 2023. For convenience, we reproduce the illustration here with parties mapped to their respective positions:

Why does this framing matter? It matters because it is the key framework that leads to a more refined interpretation of the Howey test. Under that interpretation, the “common enterprise” prong becomes moot for assets that trade on secondary markets and the “efforts of others” prong becomes moot for assets that do not generate cash flows. We elaborated on these concepts in our Binance amicus brief. More to come…

How many prongs does Howey have?

When the Ripple decision came out, we took issue with Judge Torres’s interpretation of the Howey insofar as she concluded that the test has three prongs. Indeed, the subtitle of one of our posts at the time was: Shouldn’t we all agree on the number of Howey prongs first? We said:

Here, Judge Torres lumps what is commonly referred to as the third prong, “expectation of profits,” and the fourth prong, “efforts of others.” In addition, there is no mention of fourth prong anywhere in the opinion.

We believe this is a fundamental problem.

Why? Because whether the Howey test has three or four prongs goes to the core of how Howey operates. Certainly, we believe that the “expectation of profits” prong and the “efforts of others” prong measure fundamentally different things. As such, it is perfectly possible that a certain transaction or asset fails one prong but not the other. Lumping them into a single prong, then, could lead to an incorrect application of Howey.

Eight months later, Judge Failla sides with Judge Torres in one respect: she characterizes the Howey test as a three-prong test:

Against this backdrop, the Court turns to the specific question of whether the SEC has adequately pleaded that Coinbase intermediated transactions involving Crypto-Assets that suffice to constitute “investment contracts” under the three-pronged Howey test. Because Defendants do not dispute that purchasers of the Crypto-Assets make an “investment of money,” the Court’s analysis focuses on the two remaining Howey prongs.

She does so, despite the decision later citing the work of the Crypto Rating Council (“CRC”):

The CRC subsequently released a framework for analyzing crypto-assets that “distilled a set of yes or no questions which are designed to plainly address each of the four Howey test factors” and provide conclusions regarding whether an asset has characteristics strongly consistent with treatment as a security.

Indeed, the CRC is very explicit in its position that the Howey test has four prongs:

Within the same decision, Howey is characterized as having both three and four prongs, which, honestly, doesn’t make much sense to us. The Howey test is not only pushing 80 (if it were a person, it would be a long-living person), but it also has been the undisputed legal framework used to resolve investment contract-related disputes. It would be strange to not agree on whether or not a person is missing a leg at the ripe age of 80. It feels equally strange that there is still no consensus on how many prongs Howey should have.

One could dismiss our concerns as minutiae and argue that the fourth prong is unlike the left leg; the third prong and the fourth prong are doing the work together, and by combining them and treating them as a single prong, one does not materially change the Howey inquiry. We wholeheartedly disagree. The fourth prong is very much like the left leg; it is needed on a stand-alone basis. We strongly believe that the fourth prong is about the cash flow generation potential of assets and those assets are the only ones that one can potentially invest in. If an asset does not generate cash flows, one can only speculate on them, not invest in them. As such, a Howey inquiry into an asset that does not generate cash flows should be done with the fourth prong “turned off.”

What does that mean? One helpful analogy could be the determination of residency for tax purposes in the U.S. One is considered a resident for tax purposes if an individual has either a green card or alternatively, meets the so-called substantial presence test, which measures how long one person spent time in the U.S. Not having a green card does not mean one is out of the IRS’s crosshairs. Even with the green card prong “turned off,” the substantial presence test can still lead to an outcome in which one is considered a resident for tax purposes. The two tests are not applied in conjunction, they are applied separately. We believe Howey is similarly non-conjunctive, but unlike the tax residency test, the “investment contract” test is not clear.

If Howey is meant to be non-conjunctive, why didn’t the Supreme Court say so? The answer lies not just in legal principles but in financial history that led to those principles. Practically all investment vehicles at that time were assets that generated cash flows. It is the “financial innovation” in the 21st century that exposes the ambiguity in Howey.

Why does applying Howey conjunctively cause a problem? It is as if the IRS required individuals to be green card holders and spend enough time in the US to determine tax residency. Not having a green card would amount to sidestepping tax obligations because it would lead to the determination that one is not a resident for tax purposes, also leading to a smaller tax base. Making the tax base smaller in this fashion wasn’t the policy, so the rules of the road are clear with respect to the determination of tax residency. In the same way, a conjunctive application of the tax residency test would make the tax base smaller, the conjunctive application of Howey makes the universe of investment contracts smaller. Purchasers can expect profits all they want, but a perceived lack of “effort by others” would deny them the protection they need.

So, if conjunctivity is the real issue, why is combining the third and fourth prongs into one prong problematic? It is true that the conjunctivity issue does not go away even if one acknowledges that Howey has four prongs, but the combination of two prongs into one creates a further complication: It effectively forces Howey to be conjunctive. When the prongs are applied separately, it’s now possible to create a mindset where one has to think critically about each prong. Having four prongs is more flexible than having three, and that mindset is a much better foundation for interpreting Howey the right way. The acknowledgment of having four prongs allows us to see better that conjunctivity is the problem.

Combine the prongs, on the other hand, and it conceals the issue even more. It creates the illusion that a transaction in an asset that does not generate cash flows does not constitute an investment contract if the profits do not depend on the efforts of others, regardless of what the buyers’ expectations are. With four prongs, there exists a path to properly refine Howey. With three, that path, which is already hard to see, becomes even more invisible.

With billions of dollars and investor protection on the line, we absolutely believe Howey needs consensus. The Supreme Court intended Howey to be a flexible test. Non-conjunctivity makes it more flexible, and the acknowledgment of all four prongs (as opposed to three) is what allows us to better see the conjunctivity issue. The overarching question is this: If people believe that they are investing when they are actually speculating, should they be protected? We believe they should.

This is the story behind our cover image today: The crypto industry is choosing the path on the far right. With this decision, the court chose the middle path, which was the right outcome, but truly sunny days run through the path far left. The Howey refinement we are proposing is the legal theory that would put society down the correct path.

These ideas of ours will take time to gain acceptance and there will likely be disagreement on what the fourth prong accomplishes. However, there shouldn’t be any disagreement on how many prongs the Howey test has. We should start there and then sort out our disagreements on what the prongs actually accomplish.

Offeror Behavior Is A Poor Proxy for Buyers’ Expectations

In the decision, Judge Failla hones in on three teachings of the relevant case law. First:

To begin, there need not be a formal contract between transacting parties for an investment contract to exist under Howey.

We fully agree with that; we argued the same in our amicus brief. Second:

Next, when conducting the Howey analysis, courts are not to consider the crypto-asset in isolation. Instead, courts evaluate whether the crypto assets and the “full set of contracts, expectations, and understandings” surrounding its sale and distribution — frequently referred to using the shorthand “ecosystem” — amount to an investment contract.

This one is more nuanced. We agree with the holistic nature of the evaluation, but the ecosystem description is a slippery slope, which Coinbase can be expected to exploit by pointing out some loose ends when comparing Bitcoin to other cryptocurrencies More on that the next time. Third:

Finally, in assessing the circumstances surrounding the sale of a crypto asset, courts should look to what the offeror invites investors to reasonably understand and expect. To do so, courts examine how, and to whom, issuers or promoters market the crypto-asset.

Courts should look at that, sure, but should not take their findings as dispositive. The third prong of the Howey test is about the buyers and their expectations, not the offerors and how they promoted the assets. Looking at the offerors is more of a practical necessity. It is difficult, if not impossible to understand buyers’ expectations, and there are significant line-drawing problems. One court actually considered an alternative: could all purchasers be dragged to court, put under oath, and explain why they bought it? Yet another interesting thought experiment came from Mark Cuban, who suggested that looking into the blockchain could help understand buyers’ expectations.

So, the conduct of the offeror could be a proxy for understanding buyers’ expectations, but it is a poor proxy, especially with digital assets. When the Howey test was conceived, the Supreme Court couldn’t have expected this digital age nor anticipated how it could apply in this digital age. That doesn’t mean that Howey is wrong, it just means it is about time to recognize the nuances underneath it. As long as the car works, one can keep driving it. If there is a setback, one doesn’t need to sell the car or ignore it. One may just need to open the hood, make the necessary repairs and get it safely back on the road. This is exactly where the legal community finds itself.

So, what is the problem with focusing solely on the offerors? First, it lends credence to the idea that when there is no offeror, it would be difficult to find a security. The SEC itself seems to be under that impression, which may have led to them characterizing Bitcoin as a non-security (we disagree). Second, it incentivizes the digital asset community, pushing it in the wrong direction which may lead to it being used as a roadmap.

What could that roadmap look like? One can read Judge Failla’s decision, pick out the advertising statements that are considered problematic, and go the other way. In a world where the large majority of the finance community concluded that Bitcoin is an investment despite Satoshi himself not being comfortable with it, the promoter (or offeror if one exists) of a digital asset does not need to work as hard as someone who touted stocks a century ago. One could pitch crypto as “the future of money” or whatever, and speculators fancying themselves as investors would simply pay lip service, though their true motives and/or expectations might still lie on the side of profit-making. The need for investor protection remains, but a siloed focus on the offeror side could deny the investing public the very protection they need.

How will Coinbase respond? In many ways, we don’t think their strategy has changed. We still expect them to point out certain inconsistencies between the SEC’s Bitcoin treatment and other digital assets. We also expect them to continue to harp on commodities and collectibles. We will explore these ideas further in our next post.