Kalshi v. CFTC - Round 1

Part III - The Picture

Mark Twain reportedly said:

The difference between the almost right word and the right word is really a large matter. ’tis the difference between the lightning bug and the lightning.

Such is the case with legal case visuals. We believe there is a single picture in every legal dispute that neatly summarizes the parties’ positions. Moreover, the difference between the almost right picture and the right picture is really a large matter.

It is not easy to produce that picture, but once it is produced, it holds the keys to an unparalleled understanding of what’s at stake.

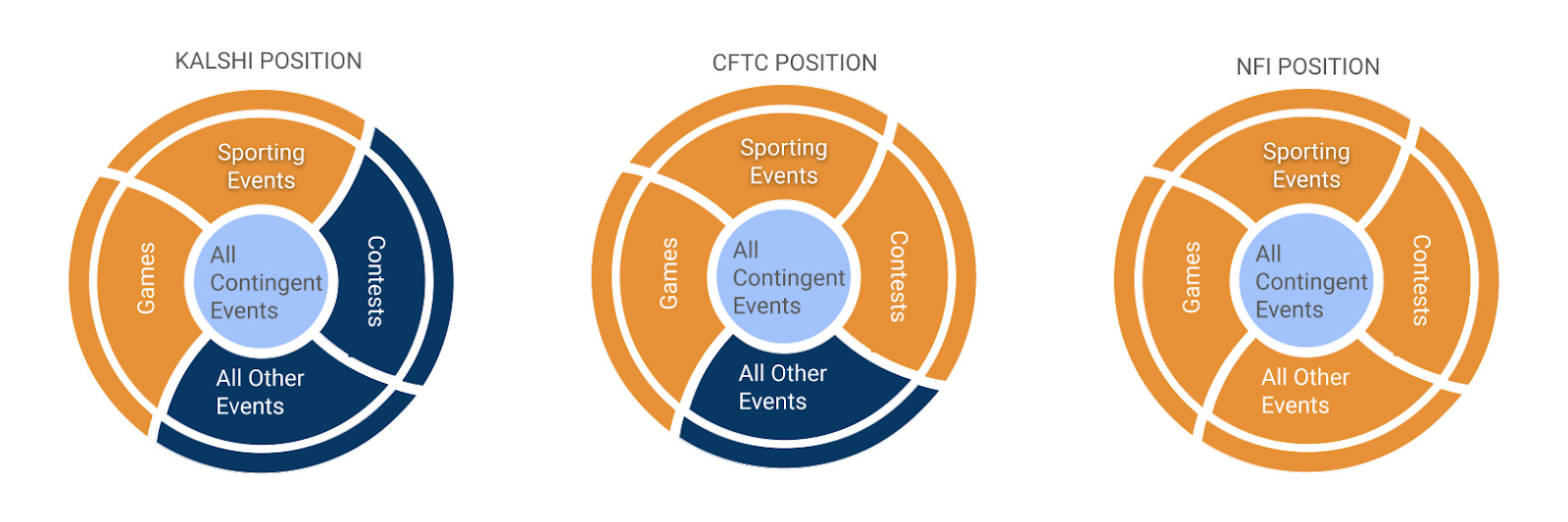

This 2x2 table was the picture that best summarized the SEC v. Coinbase litigation. We then filled in the blanks, and placed the parties in those four quadrants.

It may take a while for this picture to break through, but once it does, it will be so obvious that people will look back and say “wait, the court knew this but it still ruled the way it ruled?”

Let us take a stab at it again, this time for Kalshi v. CFTC - Round I. In the graphic below, the orange color represents the extent of the CFTC’s authority when it comes to event contracts

Are you not entertained? Read on, especially if you are a stakeholder or litigator who wants to test the legal system, this time with an argument that, in our opinion, holds together quite well.

Shouldn’t this case have been about whether or not election market contracts serve a genuine economic purpose? It seems that even Kalshi was expecting a battle along those lines. After all, the phrase “economic purpose” features extensively in their July 2023 comment letter to the CFTC. For example:

Congress has repeatedly recognized that futures and other derivative contracts serve economic purposes and, therefore, state laws that purport to prohibit or regulate futures or derivative contracts (including gaming laws) do not violate the CEA and are preempted. All of this shows that Congress and the states understand that there is a critical distinction between betting and legitimate, federally recognized and regulated financial activity. Election contracts that are designed for price formation and hedging on a derivative exchange constitute legitimate financial activity.

And:

1: The contracts have a strong economic purpose.

The hedging and price basing use cases are myriad and would allow individuals to take advantage of a product that is currently strongly in demand. Elections cause extremely large economic impacts and are some of the biggest risks that many businesses will ever face. This is detailed at great length in Kalshi’s submission and has been validated by dozens of public comments from retail, business, academia, and members of industry, including Kevin Standridge, Sam Altman, Geoff Ralston, Robert Orr, Valentin Perez, Robin Hanson, James Bailey, Rohan Palvulri, Jason Crwaford, Dustin Moskovitz, Andrew N, and James Angel.

It appears that Kalshi was ready to fight the battle along the lines of economic purpose.

If that ended up being the main disagreement between the parties, we wouldn’t be writing a long series about this case. Our skepticism that election markets serve a genuine economic purpose aside, if the Commission truly believed that they do, then the proper thing to do would be to allow the listing and trading of the contracts. The Commission, after all, made a similar determination with respect to box office movie futures many years ago, before Congress eventually outlawed those contracts.

However, that’s not what happened. The CFTC, willingly or otherwise, turned the case into a major disagreement about one word: gaming. That could have been the winning strategy if the CFTC interpreted the Dodd-Frank Act how we do:

By gaming, Congress actually meant gambling;

All contingent events are in play; and

The Economic Purpose Test, while repealed, should still be the guiding principle.

Instead, this is what the CFTC did:

They adopted #1; but

Contradicted that position by refusing that all contingent events are in play; and

Offered reasonable arguments regarding economic purpose, but because they narrowed down the definition of “gaming,” they effectively allowed the court to decide the case without even considering economic purpose.

That’s Kalshi v. CFTC - Round I, in a nutshell. In the rest of this series, we will elaborate on these ideas.