Origins IV: The New Sports Economy Experiment

How a mission to teach finance through sports ultimately tested securities law

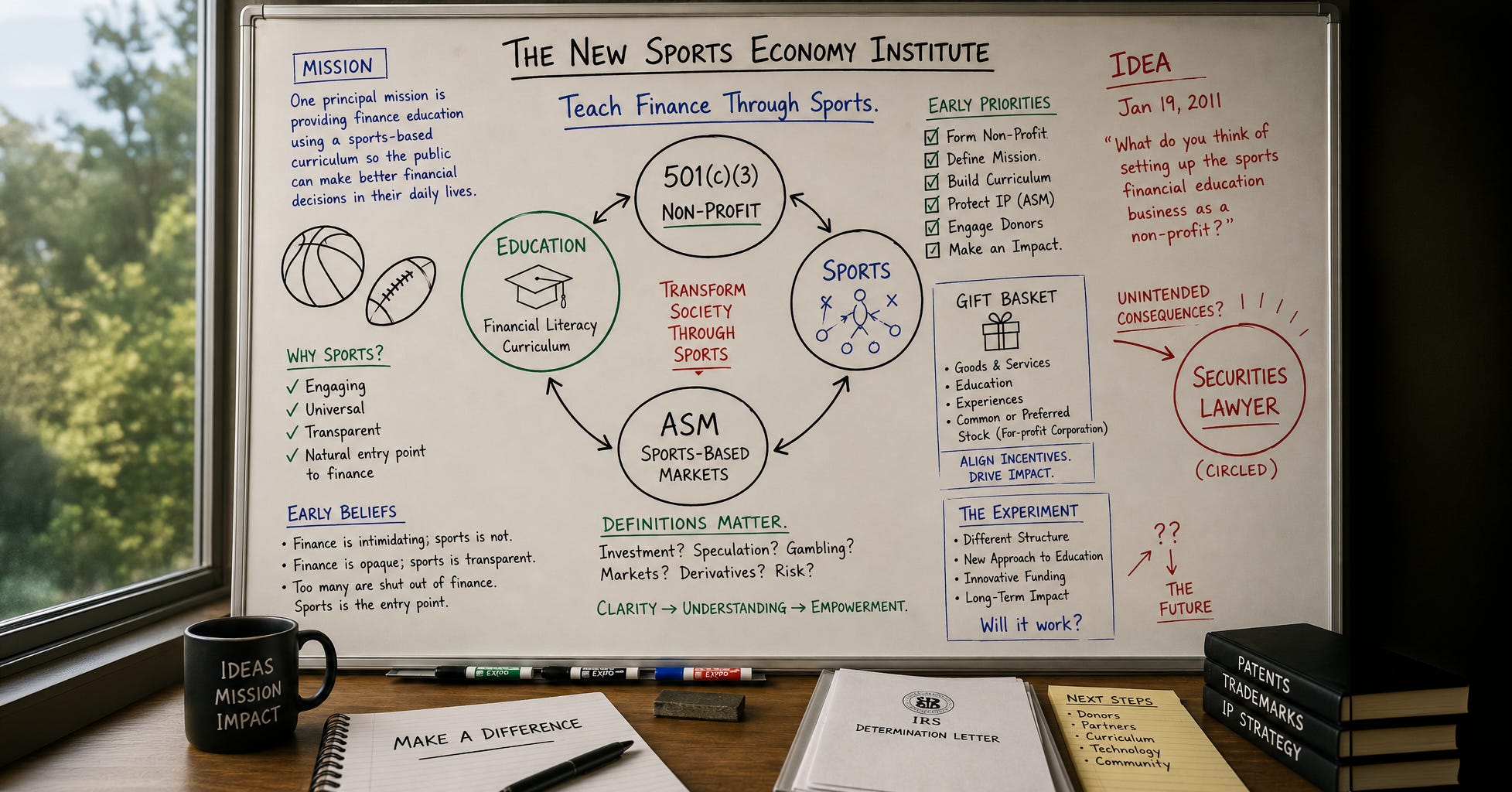

Jan 19, 2011. Chris had an idea, which he summarized in an email he aptly named… Idea. He opened with:

What do you think of setting up the sports financial education business as a non-profit?

Fresh off his Chapter 7 personal bankruptcy filing, he was looking for a fresh start. I could tell his brain was in overdrive. That’s Chris. He doesn’t rest. He is constantly thinking, exploring, trying to find the next move. As I shared with you in Origins II, that’s how he pivoted from ASM to SRI. And now that SRI was off the table, he was plotting out what would come next.

I was skeptical at first, and I knew nothing about non-profits. At the same time, I was looking for a home for some of my own ideas. I wouldn’t say I truly understood how important definitions were back then, but my instinct was: People were talking past each other because they didn’t agree on what basic financial terms meant. Later that day, I wrote back:

On my end, the issue I was having was what to do with the amount of information (and thoughts) I have around investment, speculation, gambling, markets, role of derivatives, sports-based markets, a new education curriculum on sports/finance etc.

Investment, speculation, gambling... The lack of consensus on these words bothered me fifteen years ago. The lack of consensus on these words is why I co-founded Lexicon Labs last year.

A few months passed, and Chris sent another email. This time, he wasn’t brainstorming–he was in full-commit mode:

I am proceeding with the formation of our 501(c)(3) non-profit: The New Sports Economy Institute as the master organization for the deployment of our educational mission.

This was on July 7, 2011. In other words, somewhere between Chris filing personal bankruptcy and the bankruptcy court deciding that the court was not permitted to review an issue previously determined by a state court in an action between the same parties. That entire chain of events is what led to me a question I thought was worthy of the Supreme Court’s attention - Origins III is that story.

I was excited. Financial literacy was top of mind for me, and I was determined to take every opportunity that might allow me to make my mark in that world. A couple of years later I also became the Regional Tax Co-lead for Earn Your Future, PwC’s financial literacy initiative, and a junior board member at Econ Illinois, an economic-empowerment non-profit. For now, though, The New Sports Economy Institute (“NSEI”) was the vehicle for me to try to do some good in the world by clearing up some confusion.

Chris completed the paperwork and a couple of days later, formed the NSEI. Its mission, in a nutshell, was Teach Finance Through Sports. The IRS papers said:

One principal mission is providing finance education using a sports-based curriculum so the public can make better financial decisions in their daily lives.

We absolutely believed that. Finance was intimidating; sports was not. Finance was opaque; sports was transparent. A small subset of the population had the opportunity to learn finance in college, but a much larger portion of society was shut out. Sports offered the best way, if not the only way, to provide a natural point of entry. And because ASM was a sports-finance invention (See Origins I), it was going to be the natural, hands-on entry point.

NSEI’s mission statement would later evolve to something even more ambitious: Transform Society Through Sports. The financial-literacy piece would eventually become one leg of a three-legged stool. But early on, it was mostly about exploring definitions

Three years later, NSEI would be officially granted non-profit status. But instead of becoming a force in financial education, it would end up making headlines in a way we did not anticipate at the time.

Why Non-Profits?

Non-profits are important vehicles for executing on missions society cares about. Harvard is a 501(c)(3). So is Mayo Clinic. The NCAA has been tax-exempt since 1956. But perhaps the closest structural example to NSEI is OpenAI. It initially started as a non-profit in 2015 before famously converting to a for-profit entity (in 2019), and setting the stage for a lawsuit for the ages between Elon Musk and OpenAI. One could say Chris envisioned something similar, just a few years earlier.

No matter how grand the vision, we don’t live in a world where enough people will choose altruism purely for its own sake. Society needs more than that. Fortunately, America realized this long ago and, through Congress, decided to give non-profits, and their donors, an assist.

Charitable tax exemptions are not new; in fact, the origins of the tax-exempt sector in the United States predate the formation of the republic. Section 501(c)(3) itself is a creature of the 1954 Internal Revenue Code.

The tax benefit was helpful, but Chris instinctively understood, not everyone responds to incentives the same way. So, he came up with an idea: Gift a basket of goods and services to NSEI donors. Part of the package included common or preferred stock of the parent company.

I cared about NSEI’s mission. I had already been contributing financially to ASM’s parent company, trying to keep patents and trademarks alive. NSEI gave me another vehicle to match my capital with the need. According to my records, on May 24, 2012, I made my first donation for $425.

2012-2013: Early Days

During 2012, I donated a total of $2,225 to NSEI. In 2013, another $6,275. The amounts were still relatively small–I had two kids in diapers at home, and I was trying to get a promotion at PwC. Later, the non-profit structure (not the non-profit itself per se) of donors receiving shares in a gift basket in return for their donations would bother me greatly, and I would decide to be quite vocal about it. In those early years, however, I may not have questioned it much, if I did, I can’t find any evidence of where I had voiced any concerns.

The story, as you will see below, evolved in a way that created the perception that Chris acted as a lone wolf and concocted a scheme when everybody else told him not to. It is true that most insiders grew uncomfortable with the donation model. But it is also true that the opposition, including me, did not become vocal until late 2014.

When the IRS granted NSEI its tax exempt status in August of 2014 (retroactively), I itemized my deductions for 2013 (I had an extension on my tax return) for $6,275 and moved on.

Early 2014: The Gang Returns

In 2013, Chris felt… hopeless. ASM was effectively dead, so was the SRI. The SCOTUS petition didn’t go anywhere. The non-profit path was motivating, but there was no light at the end of the tunnel with respect to ASM. He started praying. And somehow, the ASM band began to get back together. Ace Underhill, the technology mastermind behind the ASM platform, and everybody else came out of the woodwork. We convinced each other that it was time for another run. The app economy was now in full force, so we needed an app for ASM. For the talented Mr. Underhill (Ace), this wasn’t a problem. He built the app,and got it into Apple’s App Store. ASM Free was born. The idea was twofold:

Collect enough market/trading data to continue refining the product; and

Use it for educational purposes and integrate it into the NSEI curriculum.

The curriculum! That was supposed to be me. I had charged out of the gate quickly when Chris first formed the non-profit, producing over 20 chapters in less than two years. But somewhere between home life, the PwC promotion, and other financial literacy efforts, I lost my momentum. In addition, my ideal curriculum envisioned using ASM itself as a learning platform, and we didn’t quite have that yet either, at least not until Ace built it.

Chris became uneasy about the lack of progress, or rather, what the lack of progress could mean for the non-profit. Was it ok to solicit donations for a financial-literacy nonprofit when not much was happening on the financial literacy front? Could the IRS revoke the non-profit status if “teaching finance through sports” wasn’t actually happening yet? So he decided to solicit some advice from an expert. Enter Jill Lublin.

Late 2014: Jill Lublin

Jill Lublin is a master publicity strategist, consultant, and bestselling author. Chris asked her what would mitigate the risk of NSEI’s 501(c)(3) status from being impeached. Lublin advised that NSEI re-donating to any non-profit would do, as long as the re-donations constituted at least 10% of the donations to NSEI.1

Upon receiving this advice, Chris began re-donating 10% of all donations to charities–WorldVision being the recipient of a vast majority of them, largely because of its powerful donation matching program. It wasn’t unusual for the donation to produce another 8x or 10x on top of the original amount.

One can argue whether this re-donation strategy was a good idea or a waste of money. What’s undeniable is that it was expert advice. It all made sense. Chris was concerned, he sought guidance, he listened to the advice and he implemented it. He followed the exact same pattern he did with the ASM. This would become quite consequential later. But just as the ASM-to-SRI pivot never made it into the California court record in the Seth Leon dispute, the true origins of the charity re-donations would not make it to another court proceeding–because years later–one attorney would convince herself that none of that mattered, and telling that story wasn’t in the company’s best interest when in fact it clearly was.

Late 2014: My Tax Return Inquiry & Growing Concern

According to my records, I would end up donating $54,722.11 to NSEI during 2014. This was a big number, and I wanted to make sure I had the correct tax treatment. I was a tax consultant myself, so I understood I needed expert advice.

I presented the information to my tax advisor and he looked at the facts and told me that I was simply being gifted shares by a non-profit. I explained that the non-profit and the for-profit companies were controlled by the same people. That didn’t change his conclusions. In his professional opinion, I was making donations to a non-profit designated as such by the IRS. The non-profit could absolutely gift me shares, and it was my right to claim the tax deduction. In any event, it was likely more a valuation question anyway, the same way one can only claim the amount in excess of the value (a $300 donation to a non-profit is a $200 tax deduction if you get a dinner in return that is valued at $100). In 2014 at least, and largely for 2015 as well, the company had no revenue, no partnerships, no clear path to commercialization and no investor in sight. One could argue that its valuation at the time was de minimis.

I followed the advice. But I started getting uneasy regarding another matter. Could the gift-donation model be construed as a securities offering in disguise? The thought began to bother me more and more so I decided to become vocal about it.

PwC taught me many things, one of which is leaving a trail of important conversations. I don’t recall why I felt a higher level of risk, but around October 2014, I was concerned that the SEC could come after the company alleging an unregistered securities offering. In an email dated October 27, 2014, I said:

I am by no means an expert in the area. But I understand enough that I realize we need an expert. We badly need a securities lawyer, NOW.

And:

I truly believe that violating the laws is not the intention here, but that’s not an excuse.

So, I didn’t think Chris was willingly violating the law. I had actual past behavior to rely on: When his counsel, Paul Architzel, advised him to pivot out of ASM, he complied. When Paul Architzel asked him to stop accepting deposits from U.S. traders, he complied. When Jill Lublin wanted him to re-donate 10% of all contributions to any charity, he complied.

He would later testify that if a securities counsel advised him to stop putting stock in the gift basket for the donors, he would. And I believed him; he had done that at least three times before, and I had no reason to believe that he would start dismissing professional advice.

Yet I felt he didn’t assign the same weight to some of my own assessments. At one point he had asked me whether I could point to any case law that spoke to the structure he had implemented. Arguably, this would have been a job for a lawyer or paralegal, but Chris had confidence in my research skills. I wasn’t able to uncover anything that had this same fact pattern. I believe that’s where Chris and I began diverging substantially. For me, absence of evidence wasn’t evidence of absence. The fact that the issue wasn’t yet tested in court (if true) wasn’t determinative at all. I understood that substance triumphed form, and it was at least conceivable that some people were donating because of the corporate shares they were receiving in return.

To Chris’s credit, he wasn’t dismissive of the idea of engaging securities counsel. He said:

We will hire a securities lawyer but not now. I have it on my whiteboard as a priority.

That gave me some relief. I responded:

Good to hear that a securities lawyer is a priority. I think we all agreed on that point. It could be a very cheap solution to potentially much bigger problems down the road, which I think is where our disagreement lies. This is not a big job, nor is it necessarily expensive. But it’s very valuable insurance and I recommend that we button this down as soon as we humanly can.

Chris replied:

It has been on my whiteboard as a priority for many months.

The company would engage a securities lawyer later for another purpose, but never to stress-test the theory that a non-profit could grant shares of an affiliated for-profit entity in a mixed basket of goods and services in return for donations received. Instead, that question would eventually be tested in court.

Why Do People Donate?

The email chain I quoted from above was quite long. I was very concerned, so I didn’t let it go:

Arguably people are making those donations because that is the only way to buy shares which would make this effectively a securities offering.

Why did people donate to NSEI? Did they not care about the mission and just want the shares? What motivated them?

To Chris’s credit, a later survey of donors would reveal that only 8.1% of them did so for the sole purpose of obtaining corporate stock and the rest had, at least partially, other motives. Intent is hard to measure, and one can never know whether people themselves revealed their intentions accurately, but if they did, it was far from automatic that everybody viewed this as a securities transaction.

2015-2016: The No-Action Relief Request

The uncertainty around the gift-donation model was not resolved in 2015. My donations grew even more substantially to: $78,317. Now, a really large number, I checked with my tax advisor again. The advice remained the same: Take the deduction.

I did some independent research and concluded that payments made directly to third parties on behalf of the non-profit were more risky. I’m not sure I actually got that right. But that was my assessment at the time, and I decided to not deduct everything, telling my tax advisor:

I am not comfortable taking the non-cash deductions to charity (the payments I made to third parties on behalf of the charity). While I understand that there is a position that these can be deducted, I read quite a bit of case law while I was at vacation (yes, I am a nerd I guess!), including a Supreme Court Case, and I find that position as risky based on my reading and fact patterns in the case law. I am willing to receive a reduced refund in exchange of lower risk. As such, I want to deduct only direct cash contributions.

The bigger issue remained. Could the gift-donation model be construed as a securities transaction in disguise?

In any event, we needed to showcase a real-money version of the product and we needed to get moving on the regulation front. But how?

We decided to put together a no-action relief request letter to the SEC. The gist of it was: We believe ASM should be a regulated exchange, we believe what we are offering are securities, we just quite don’t know how to do this, so please guide us. Here was our key ask:

Importantly, we don’t envision the no-action, if granted, serving as a perpetual placeholder for our proposed, limited market operations. On the contrary, we view it as an intermediate, transitionary phase on the path to full regulation. It is our intent during this phase to:

i) collaborate with the SEC and other regulatory agencies, as needed, through a continuous and transparent dialogue to determine the details as to how the proposed sports stocks and the concept of sports investing should ultimately be regulated; and

ii) to demonstrate the benefits of sports investing to the world, not only as a needed addition to capital markets, but also how it can become an enabler of global economic development and educational reform.

What did we mean by “limited market”? It was an act of restraint–self-imposing annual investment limits as a good-faith effort.

The full letter - if you are interested is below:

For good measure, the company also added disclaimers to its website that were honest and accurate (an excerpt is further below). Most every company in this situation takes a different approach. They go out and unleash a full market and deal with any legal problems later. They claim they don’t need regulation, let alone proactively reaching out to the regulators. NSEI had self-imposed investment limits on the ASM platform, reached out to the SEC and asked for guidance.

As they say, no good deed goes unpunished. But first, a Christmas Story.

Scut Farkus

Zack Ward is no stranger to the camera. He played Scut Farkus, the iconic red-headed bully in A Christmas Story as a child actor. Every Christmas, networks run the movie on a 24-hour cycle, and Zack–already popular–gets a fresh boost in visibility.

Chris understood that star power matters. Ace knew Zack from Hollywood, and he got involved. Chris signed an agreement with a Hollywood public relations agency, and they got to work. First came some interviews and newspapers. Then the big prize.

Squawk Box.

This was prime time TV. If you are involved with financial innovation like we were, you need to get up there. The company’s goal was to make sports an asset class, and we felt we had the goods to prove it.

Zack is extremely smart and not shy in front of the camera. But financial innovation requires prep, so I and the rest of the team helped him get ready for the big moment.

On December 11, 2017, the cameras rolled:

Perhaps not Zack’s best performance, but he did quite well. And it did bring in some traders to the website. I don’t have the official count, but I recall the number being near 2,000. We went in with 5,700 active traders if memory serves right (unfortunately Zack fumbled this number stating it as 57 and garnering funny looks from Melissa Lee, one of the hosts), so another couple thousand was meaningful.

Unfortunately, with all that attention came another massive development: An SEC lawsuit.

The SEC Lawsuit

First, it was a call from the SEC. Chris told me that they requested that Chris remove the disclaimer ASM was using on its website. This is, in pertinent part, the copy that I believe was posted at the time:

NSEI has applied to the Division of Trading and Markets of the U.S. Securities and Exchange Commission (“SEC” or “Commission”) to not recommend enforcement action to the Commission under Section 15(a) of the Securities Exchange Act of 1934 (“Securities Exchange Act”) in connection with the proposed sports-related financial instruments offered by the New Sports Economy Institute (“NSEI” or “we”).

Neither NSEI, nor Crystal World Holdings, Inc. is registered as a broker/dealer with the Securities and Exchange Commission (SEC), Financial Industry Regulatory Authority (FINRA) or any other federal or state securities regulator. At the present time, NSEI HAS NOT filed a registration statement (or a prospectus) with the SEC for any securities offered on the ASM platform. Investment products listed on the ASM platform are non-registered securities; meaning, they have not been registered with any state or federal securities registration authority.

I didn’t know what to make of the SEC’s request. To me, it was really important that the traders were not being misled. The first question we almost always get from league partners, potential investors, etc., is: Is this regulated? That is understandable. Leagues want to know whether the product went through the rigorous process of establishing regulatory certainty. Same for potential investors. The company intended to go through the process, but it hadn’t yet, so it did what it was supposed to do: Be honest about it.

You probably know this but disclosure is at the heart of everything the SEC does. The Great Depression happened, and about half of the newly issued securities were deemed worthless by Congress because of significant gaps in disclosures. The twin acts of 1933 and 1934 arose to fill those gaps, and when FDR instructed Congress, he honed on this core philosophy:

Of course, the Federal Government cannot and should not take any action which might be construed as approving or guaranteeing that newly issued securities are sound in the sense that their value will be maintained or that the properties which they represent will earn profit.

There is, however, an obligation upon us to insist that every issue of new securities to be sold in interstate commerce shall be accompanied by full publicity and information, and that no essentially important element attending the issue shall be concealed from the buying public. (emphasis added).

Courts understood this too. The Supreme Court opined (in 1963):

[W]hat is required is “a picture not simply of the show window, but of the entire store . . . not simply truth in the statements volunteered, but disclosure.

The no-action relief request, the disclosure on the website…. From Chris’s perspective–and it’s difficult to disagree with him on this one–he was showing the entire store.

Not that it always helped the company. In at least one instance, it prevented it from securing capital. The NSEI donations did bring in some funds, no question. But both NSEI and CWH constantly tried other ways, too. NSEI applied for multiple grants. There was a section 506 raise at one point. And there were crowdfunding attempts–WeFunder and StartEngine. The latter didn’t come through primarily because the platform took issue with the disclosure, more specifically the fact that the company may be offering unregistered securities. Their thinking was exactly backwards: The company tried to explain that the main reason for the fundraise was to hire regulatory counsel (as it had a decade prior with the first iteration of the ASM, and later the SRI) and to seek regulatory certainty. The disclaimer was not: “Here, get some unregistered securities.” It was: “We think these might constitute securities offerings, and we wanted to be honest about it. Until we figure it out, we want to make sure you are not misled.”

The daily fantasy sports industry did the exact opposite a couple years prior, and crypto would do the exact opposite a few years later–behaviors I never agreed with. But can you blame them? The laws say we want you to be honest. That is literally what FDR instructed Congress. That’s what SCOTUS said. But the market is not designed to reward that behavior. In our case at least, it did the exact opposite and I don’t think we were alone. In hindsight, we could have been better off if we had: i) Said nothing, or worse ii) Openly denied that what we were offering could be securities even though that’s what we believed. Something is fundamentally wrong with that picture.

In any event, the SEC did not like the disclosure, and Chris complied. Then came the Wells Notice–the dreaded document that signals litigation is about to commence.

The company responded to the Wells Notice. If there was any glimmer of hope that the SEC would backtrack (I did some research on this at the time and remember that roughly 20 percent or so of cases stop short of litigation), that hope was gone when the complaint dropped on August 19, 2019.

A Long Cycle

Litigation is very time consuming, it is expensive, and oftentimes a lot of collateral damage. For large companies, it may simply be a line item as a cost of doing business. For small ones though, it’s closer to a death knell. Just one example: The company was trying hard to catch up with its financial books and had even hired an audit firm. Once they heard about the SEC complaint that was filed, there was no effort to understand the company’s side of the story or an effort to deliver what they were contractually delivered to do and they backed out of their contract without a refund.

I was appalled. I worked for one of the largest accounting firms in the country at the time. It didn’t occur to me that service was optional for a paying client. PwC took the high road on these matters–we provided the service even if the client was behind on payments. Litigation is a fact of life. Accounting firms don’t just drop an engagement, much less after being paid in full, simply because there is unresolved litigation. That just doesn’t happen.

The whole thing felt so unfair. The company had been dinged twice. It paid but never received the service, and because it didn’t receive the service, it appeared as though it was shirking its compliance obligations–not a great look when you are in court with the SEC because of a compliance problem.

One way or another, counsel was needed to resolve the dispute. I remember speaking to one prospective attorney, and their proposed strategy was: “Throw Chris under the bus.” I told them I would be on the side of truth, and wasn’t interested in character assassination of any kind. Lay out the facts, including my internal disagreements with Chris? Of course. Purposefully tell a one-sided story just to win? I won’t do that, ever. That’s not me. I also saw how Leon did that and how that story ended. My loyalty is to the truth and to the truth only, and I am not interested in spinning because the outcome might be favorable to me.

The search wasn’t getting anywhere, but thankfully Jim Falvey came to the rescue. He was USFE’s General Counsel when the SRI, our other piece of financial innovation, got stopped at the one-yard line. He knew Chris, and Jim and I had kept in touch. He was a natural choice. But then, mid-litigation, he started having some health issues and realized he wouldn’t be able to keep up with the demands of the litigation. He suggested that we work with the lawyer in D.C. that had acted as local counsel previously, whereas Jim was on board as pro hac vice (since he was from Chicago), Cheryl Stein.

Working With the Wrong Attorney

Cheryl was not versed in securities law at all, but her rate was very reasonable and the company was stuck between a rock and hard place. Chad Deihl, who has stepped in as the new CEO in 2023, and I began paying her out of pocket, and we got underway.

There were several lengthy delays involved with this litigation, including the COVID pandemic and the January 6th insurrection (the criminal cases were in the same D.C. district and got bumped ahead of all the civil cases), and others Cheryl-related. To be fair, she was also going through some health issues. But it is also true that she wasn’t equipped for the job. Let’s just say she wasn’t the most organized lawyer. Time management was a real issue. I also felt she was rude, she yelled at Chad and I during an attorney-client phone call. Quite simply, I was appalled. I worked for PwC for 19 years and never once had I yelled at a client when there was a disagreement. Once you’ve delivered professional services at the highest level, your assumption is that every service provider operates the same way, but that’s simply not true. If the company had more access to cash, she would have been replaced early on. The idiom, “You get what you pay for” was in play here.

The even more profound issue here was that her mentality was also to throw Chris under the bus. Cheryl is a criminal defense lawyer by trade and it was her natural inclination, it’s just that she had never said I want to throw him under the bus. By the time I realized that’s what she had in mind all along, it was too late.

The Signs Were There

I should take some of the blame here because the signs were there. Cheryl never said that she was going to turn this into a character assassination. But I should have read the situation better.

Again, disclosure. When the other prospective attorney suggested how they planned to argue the case, at least that was honest. You could react to that and say, sorry, I’m not interested in going down that path. With Cheryl, it was never quite clear how she was going to argue it. I actually drafted most of the brief for her, and she would end up discarding most of it.

It started with bifurcation. When she suggested that we bifurcate the case because Chris’s interests and the Company’s could diverge, it was one of those things that sounded reasonable at first, in fact Chris agreed with it. What was expressed to us was that a lawyer shouldn’t be representing both the individual and the corporations together (especially when the individual is no longer acting for the companies) as it is often forbidden due to conflicts of interest; ultimately Chris needed to find his own lawyer. I’m not sure whether this was the right approach. Did I have my disagreements with Chris? I absolutely did. To this day, I still believe Chris took an unnecessary risk. But the way the disgorgement law works, the better strategy still would have been the way Jim was planning to litigate the case, as a unified front.

That may sound counterintuitive, so let me give you a couple of examples to drive the point home. Chris never had an employment agreement with the company. Of course, that’s not ideal, but if the paperwork is put aside and one looks at the actual economics of the transaction, he did pay himself. Chad and I painstakingly constructed all these records, and when all was said and done, our math told us he paid himself a little over $50,000 a year. Barely over minimum wage at the time and certainly underpaid as a resident in the Los Angeles area.

For someone who had the dual role of being a CEO of a financial innovation company and Managing Director of a non-profit, the compensation certainly was not unreasonable by any stretch of the imagination. So was that compensation a legitimate business expense? Of course it was. The question is not whether or not I agreed with Chris on everything. The question was whether the rate was a market rate. I was not aware of anybody else who was willing to do the job, much less for minimum wage, so that’s that.

Why does it matter that it was a genuine business expense? Because, generally speaking, legitimate business expenses get deducted from the math per SCOTUS guidance in Liu. Cheryl saw it differently. In her mind, conceding that quarter million dollars was smart, and a good look for the company because it showed the company’s willingness to budge. Worse, we literally had no more than 30 seconds to discuss her decision; by the time she had laid out her position, the brief was already late and needed to be submitted. In the heat of the moment, and panicking because we were late, we didn’t have an opportunity to make a healthy assessment and ended up taking a position that we (at least I) didn’t believe in.

Cheryl fumbled the non-profit issue too. I took a lot of time to piece together the facts, the audio with Jill Lublin, everything. I peppered it with some case law references, too. The question was the same. Were the re-donations a legitimate business expense? In my mind, they absolutely were. My draft said:

Charitable contributions by NSEI were effectively an insurance policy for NSEI, which paid ‘premiums’ to a non-profit of choice to avoid a low-probability, but catastrophic outcome of a potential impeachment of NSEI as a non-profit. The SEC’s position amounts to arguing that because an insurance premium does not improve a bottom line, it is not a legitimate business expense. For these reasons, the SEC’s argument should be rejected by the Court.

Cheryl ignored it. That was incompetence at best. When a CEO asks for guidance from an expert in the field, and implements the advice to manage a potential risk and uses funds for that purpose, that sounds to me like a legitimate expense. It is even more puzzling how an attorney would not see that there is, at a minimum, a plausible argument here.

A Story of Incentives

It’s an incentive story. It’s always an incentive story.

As an economist, I learned long ago that everything boils down to incentives. Back when I was a teacher–many moons ago–I taught from Greg Mankiw’s Principles of Economics. Among its core lessons, the fourth principle stood out as particularly powerful: “People respond to incentives.”

The motive is so powerful that author Steven Landsburg, in The Armchair Economist: Economics and Everyday Life, went even further and said:

Most of economics can be summarized in four words: “People respond to incentives.” The rest is commentary.

If we look at the behaviors of the parties through that lens, a picture emerges.

Let’s start with Cheryl. In her mind, she was doing the best thing for her client (the bifurcation early on, and then the strategy she followed). Many attorneys convince themselves that the client winning in court comes before everything else (that’s what they stake their business on–wins). Sometimes, they take it too far. Chad and I debated this at some point– if the client was suggesting a strategy and the attorney believed there was a better one, the attorney feels empowered to go down that path.

That level of paternalism never sat right with me. Tax consulting doesn’t really work that way. If I disagreed with my client on a position, I would voice my concern and make a recommendation, but the ultimate decision was the client’s. Why would it be the advisor’s? It’s their business, they don’t have to follow the recommendations if they didn’t think it was in their best interest. In any event, objectives should be defined by the client. Getting a true, complete narrative out was more important to me than just winning a material, yet isolated court case.

That’s my ethics line, one I am not willing to cross. But it was even worse. In this case, the complete, true narrative also happened to be helpful to the case. Ethics is enough reason, nothing else needs to be considered. But being ethical also happened to the best legal strategy for the companies; arguing that Chris actually deserved his compensation (a little more than minimum wage), or that the charity re-donations were implemented upon advice by an expert would not only be aligned to the actual facts, but it would improve the Company’s position in litigation. If you will argue against your own client, you better make sure you have true command of the situation. That wasn’t Cheryl. Her critical thinking skills were simply not there. Being a criminal defense attorney, she believed Chris was a fraud and believed the companies would be hurt in trying to align with him while bifurcated, even if Chris’s personal expenses were refunded to him from incoming donations as his form of an employee salary was the truth.

Let’s talk about the SEC for a second. Their mission, of course, is investor protection. If you have been following this blog, you know I am critical of the SEC when it comes to crypto-related matters, and that extends through the Gensler-era. My thesis has always been that crypto is not investing, and any policy outcome that doesn’t demand that disclosure, front-and-center, is a loss for America. There is a better way.

The case with the SEC, so far, hasn’t shaped up to be one where investors were prioritized. Were mistakes made? Absolutely. But how does it make sense to bury a promising company into the ground? When all’s said and done, Chad and I were both significant donors to the NSEI. If somebody got hurt, we were at the front of the line. All we want to do is to put the issue behind us and get on with the business. The vast percentage (over 90%) of the shareholders (the ones that responded to an internal survey) agreed, when they indicated on a survey that they would support the next iteration of the company under mine and Chad’s leadership. Yet here we are, still fighting and spending money, and I’m sure the SEC has much bigger fish to fry.

What was the SEC trying to do? Chris and I talked about this ad nauseum. We generally landed on the following: The SEC doesn’t want this to turn into a loophole. People are not supposed to use a non-profit/profit structure to backdoor a securities offering, and if unchecked, the structure could create a terrible precedent for society. On that we agreed. Chris actually stopped putting corporate shares into the gift basket in exchange for donations sometime in 2018, before the Wells Notice was delivered. If the goal was to “close that loophole,” I feel that could have been accomplished outside the four corners of the courthouse.

And then, there is the innovation aspect. Agree or disagree with what ASM can bring to the table, but it’s hard to deny that it is, at a minimum, a unique piece of financial innovation in the sports-finance world that deserves careful consideration. Sports investing is better than sports gambling, and we said as much in our no-action relief request:

More broadly, we believe our great nation is on a self-destructing march towards legalization of sports gambling. Through DFS, it’s already happening today. Absent an opposing voice to stop this dangerous momentum, we fear that this march will reach its final destination and cause irreparable harm to society and the sports we all love and cherish. While SEC is not responsible for creating policy, it is well within SEC’s powers to extend relief to market participants for reasonable cause. Operating under relief, in turn, would allow us to engage in a policy debate that we feel our nation desperately needs.

Those words were from 2016. I’m not going to apologize to anyone for seeing where this thing was headed, advocating for a much better alternative to gambling and asking the regulator to collaborate with us. The SEC is not legally obligated to respond to no-action requests and it was surprising for me to find that out, but the law is the law. To this day, I am disappointed as to why they never responded to it. Was it because we weren’t represented by counsel and so they simply didn’t take it seriously or was it something else? It would have been nice if the SEC, instead of taking no action on our no-action relief request, engaged with us. All the talk about onshoring innovation rings hollow when we had, and continue to have, the most interesting innovation in this space. The SEC wasn’t legally obligated to engage, but America would be much better off if they had.

Finally, Chris. We had many exchanges after litigation commenced. We never quite agreed on whether what he did was the right strategy. From my vantage point, this was all predictable. It is true that I didn’t raise objections initially. My risk antennas started buzzing later on. It is also true that I willingly participated in the donation program through the end of 2016 (In my records, I see one donation from me in 2017, and none afterwards). But I started making a big fuss in late 2014, and strongly advocated for a securities counsel. That recommendation of mine wasn’t attended to.

Why? Why did Chris and I agree on so many things, but this one turned out to be our biggest disagreement? Ask him, and he will tell you that this was the only thing that made sense. That this risk was necessary for the company to have a fighting chance. That he was the one in the control tower, not me, and things looked very differently from where he sat. He also exclaimed that he would be the one willing to fall on the sword if it came down to it.

I identified a risk, made a recommendation, and my exact concern materialized. To this day, it’s very difficult for me to even consider the possibility that Chris may have made the right decision. But the reality is we have not lived the counterfactual. Chris was adamant that was the only way the company could survive. I saw an unnecessary legal risk; he saw a necessary one. I suppose it is possible that his concerns could have materialized too if he hadn’t taken that risk. Perhaps in that world, there would be no SEC litigation. But in all likelihood, there would be no ASM either. It is true that the company still has a fighting chance of survival; a narrow one for sure. It is still hobbling, but it’s not dead.

I did get an amazing legal education out of it, and maybe that was one of the reasons. You know I don’t have a J.D.–I learned the law the way you would learn a language on the streets as opposed to the school halls. The litigation with Leon, litigation with the SEC, writing briefs, discussions with attorneys, reading transcripts; it was all part of the education.

The other result of all of this? The ASM market design was never litigated in the SEC case. Chris actually ended up not implementing the $2,500 annual investment-limit idea either, instead treating those deposits as donations. Maybe, instinctively, he realized that not only was litigation a necessary risk to take, but he also preferred a compliance litigation (a debate over securities offerings without registration) to a market-design litigation (a debate over whether SportShares are gambling or not). He, and the company, lived to tell through the Seth Leon litigation, but maybe another gambling litigation would have been too much. I can’t shake the feeling that Chris may have been, all along, trying to protect ASM from external pressure until it was ready to finally bloom.

Looking Ahead

Chris has strong feelings toward the attorney profession. Where I disagreed with him was in the generalizations. If an attorney is knowingly lying when drafting a complaint or in the courtroom, obviously that behavior is not proper.

When I read the final brief Cheryl put together–after it was submitted, the only time I read the whole thing in full–I woke up with a knot in my stomach. I wanted to puke. That feeling never fails. It’s my conscience telling me that something is off and I deviated from my internal compass. I always told Chris that I never threw him under the bus, and that was truthful. I didn’t. But I lost control of the process, and the resulting product was grossly unfair to him and largely disconnected from reality.

For starters, there were some inaccuracies in the write-up and I had the factual evidence to prove it. I requested from Cheryl that the factual inaccuracies be corrected. A simple amendment would have done it. I think she actually amended the brief but didn’t implement all my comments. In her mind, perhaps the corrections would not have helped the story she wanted to tell. For me, it has always been the other way around. If the facts don’t help me, so be it. I don’t claim to be mistake-free, but I have always tried to live a life where I don’t mind if the whole thing becomes the front page of the New York Times.

So factual inaccuracies were already bad, but there was also a bigger problem. Many relevant facts didn’t make it into the brief at all. Most of the valuable context was lost. The same way Leon was successful in painting a picture of Chris running a bunco operation and gambling scam, the company’s own counsel was able to manufacture a perception that was somewhat similar.

It was too much for me. I was never an employee or a formal advisor of the company even after Chris stepped down at the end of 2022. Chad is the CEO and I had been funding the litigation, hoping that the issues could be resolved so we could get back to business. Because of how the litigation transpired, with the process going in a direction that I was absolutely not comfortable with, I told Chad that I was out and would not be funding the litigation further.

Chad and Paul, a longtime ASM supporter and an informal advisor, took a different view. After I had stepped out of the process, they spoke to Cheryl and she explained to them what would give the company the best chance to win. I wanted to part ways with Cheryl, they elected to continue. They held the position that it was too far along in the litigation that the judge would not have allowed a change of attorneys anyway. I don’t blame them for their decisions, and I still work with Chad every day and will likely add Paul to the roster again at some point. I understand they were trying to find a glimmer of hope somewhere, a life jacket of some sort. We have been through so many trials and tribulations, it certainly is exhausting after a while simply trying to do the right thing only to hit another obstacle. I suppose that’s why they say that overnight successes were 15 years in the making.

All that said, it was obvious where the whole thing was headed. A badly told story, disconnected from reality that suggested Chris was a villain, it was obvious to me that the approach would not result anywhere close to a successful resolution. Best for the client? Not even close.

At the end of the day, I was proven correct in my own legal assessment. The D.C. District Court handed the SEC a judgment for the full amount of disgorgement based on D.C. precedent, but it did offer a glimmer of hope when reducing the penalties by 91%. All in all, it was still much heftier than we were all hoping and Chris was handed down a penalty of his own.

One day, Chris may be proven correct about his survival assessment. It is possible that one day, we will all look back and understand that the world has what it needs and if it wasn’t for Chris and his choices, which at the time certainly felt like reckless behavior, ASM would have been dead.

We’re not there yet. ASM still has a ways to go. The litigation is still in appeals and unresolved. I am back on board with ASM and we have hired professional securities counsel to represent us, arguably where we should have been all along. We are also constantly searching and making more connections in the sports-finance world.

It has been a long road. A very long one. But we are all unified and marching toward the same goal.

Most importantly, there’s still hope. Sometimes, that’s all you can ask for.

Chris would later recount the conversation in his testimony: “She’s like, ‘... You have to take some portion of your donation income and redirect it to a registered charity. You can pick it. It doesn’t matter which one it is.’ I said, “How much?” She said, “10 percent, at least 10 percent. Redirect it to some charity that you pick so that you have an immediate charitable benefit on the way to your bigger goals.”