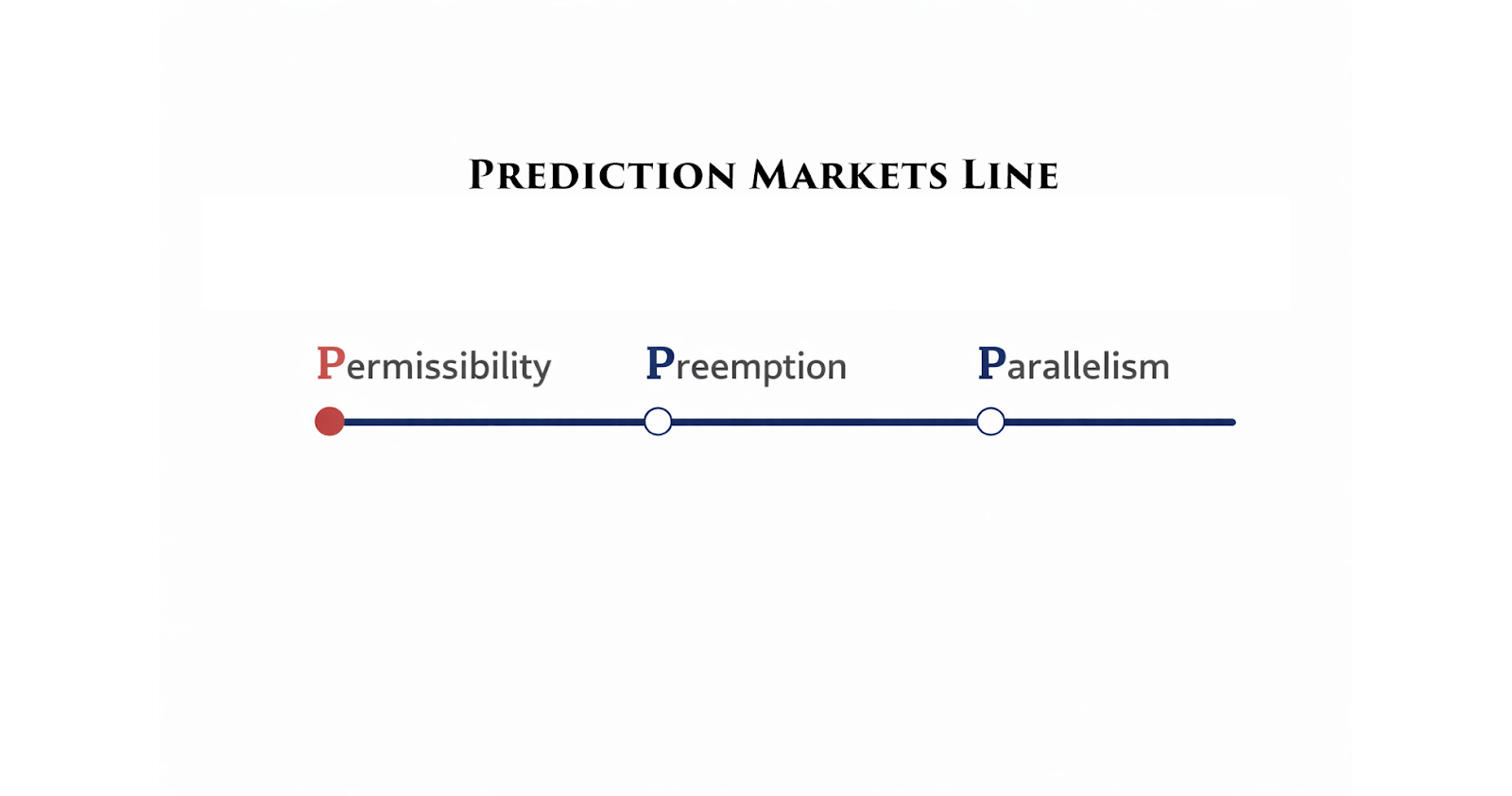

Litigation Sequencing — Stop #1: Permissibility

The threshold battle over whether prediction markets have the right to exist

In yesterday’s post, I introduced the idea of litigation sequencing—the observation that in complex regulatory disputes, the most important question is often not who is right, but which question gets answered first.

This week we are focusing on the prediction markets litigation that is unfolding across three specific stops, which I call the 3P Framework, each bringing the industry closer to its final destination, SCOTUS (unless SCOTUS intervenes earlier):

Stop #1: Permissibility

Stop #2: Preemption

Stop #3: Parallelism

Today we will focus on Stop #1: Permissibility, and then finish out the week with the other two.

The Threshold Question: Do Prediction Markets Have the Right to Exist?

The litigation sequence began with a foundational question in KalshiEX LLC v. Commodity Futures Trading Commission: Are the election markets contracts allowed to exist at all under the Commodity Exchange Act?

When the CFTC blocked Kalshi from listing congressional control event contracts, the dispute was not about preemption, state gambling laws or the structure of the sports betting market. It largely turned on the meaning of a single statutory provision: The Commodity Exchange Act’s discretionary authority over certain contracts involving “gaming.”

Late 2023 was a permissibility battle. This was the landscape:

Two Ways to Fight the Permissibility Battle

As we explained in our previous post, there are two ways to litigate permissibility:

Approach #1 (broader): Argue for public interest

Approach #2 (narrower): Zoom in on “gaming”

For decades, the CFTC relied on Approach #1:

In 2012, the CFTC denied Nadex on the lack of public interest grounds;

In 2021, ErisX ultimately saw the same writing on the wall and withdrew their contracts; and

In 2023, Kalshi was denied on exactly the same grounds–prompting their lawsuit.

Kalshi likely expected a public-interest fight. They even sent a letter to the CFTC touting the economic purpose of election contracts.

But, that’s not the fight the CFTC opted for.

The CFTC Abandons Its Own Playbook

Instead of defending the public-interest standard, the CFTC pivoted. Section 5(g) had been repealed in 2000, but the agency continued to rely on the economic purpose test for another 23 years. It was the CFTC’s North Star–until the Kalshi litigation, when the Commission abruptly abandoned it.

Why the shift? It’s unclear.

Deregulatory winds? Trump was not yet reelected for a second term back then. But arguably, the deregulatory winds were getting stronger even under the Biden administration, and perhaps there was some anticipation that if Trump were to be elected, they would be even getting stronger. It is entirely possible that the Commission concluded trying to be the last cop standing was going to be a futile exercise. If that was the expectation, it ended up being on point. Trump was elected, deregulatory winds have gotten stronger1 and CFTC enforcement has gotten weaker.2

Internal disagreement?

Commissioner Quintenz had suggested the statute was unconstitutional or at least unenforceable.3Regulatory confusion?

Bloomberg reported that staff struggled with basic questions: What is “gaming”? Does the CFTC have to consider public interest? How would they measure it?4Strategic miscalculation?

Perhaps the CFTC expected deference under Chevron–before Loper Bright changed the landscape.

Whatever the reason, the CFTC adopted an approach that was, in Kalshi’s words, an “intermediate approach [that] fits” (the CFTC’s position was lazy–it didn’t commit to any coherent legal theory) and “too clever by half” (it was strategically cute, intellectually contorted and ultimately, self-defeating).

They didn’t take Approach #1.

They didn’t take Approach #2.

They took Approach #1.5.

Under the CFTC’s theory:

They had no authority over event contracts on interest rates, inflation or weather; but

They did have authority over event contracts involving sports, elections and Academy Awards.

It was a bespoke interpretation–one that appeared to be crafted for the moment rather than one grounded by statute.

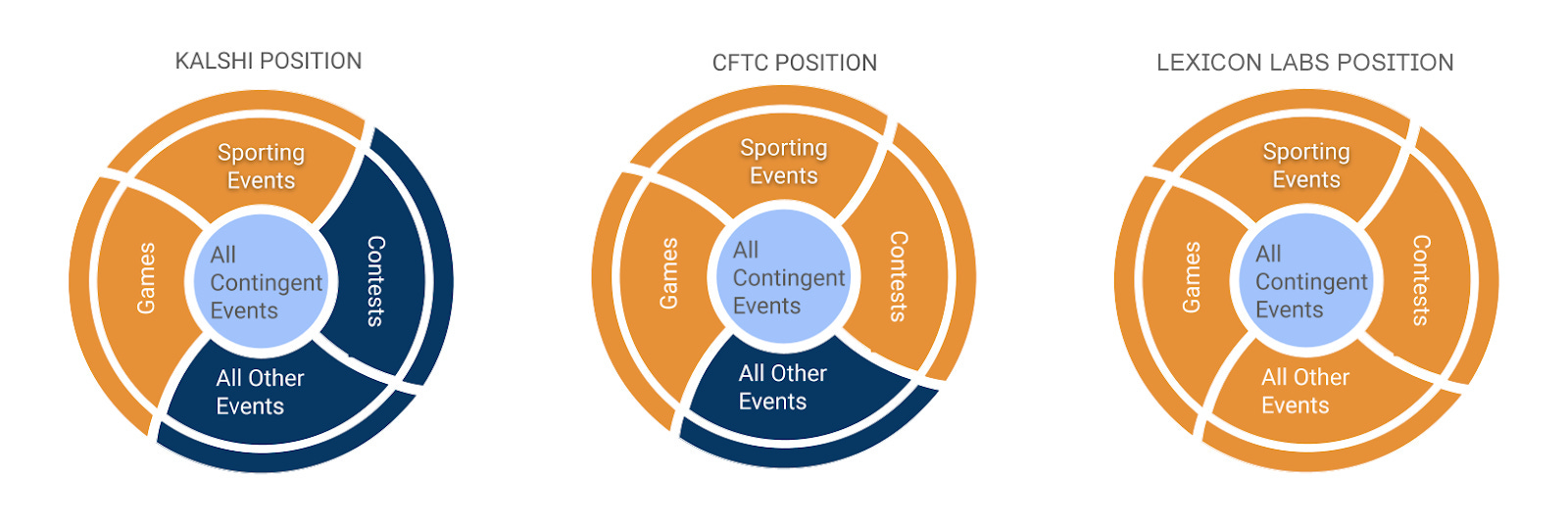

Kalshi’s Unexpected Gift

Consider this infographic that we created more than a year ago:

Going from narrow to the most broad (left to right):

Left circle: Approach #2

Middle circle: Approach #1.5

Right circle: Approach #1

For Kalshi, this was a gift from the heavens. I doubt they were expecting it. Had the CFTC adopted Approach #1, I believe Kalshi’s position would be weaker than the Commission’s. With the CFTC adopting Approach #1.5, the tables turned. Unforced error? The CFTC’s position was now simply weaker than Kalshi’s–and in litigation, that’s often enough.

Litigation is not a philosophy seminar.

Too often, it functions like a football game. One of the sides has the better case.

So, the argument that prevails isn’t always the argument that makes the most sense in the broader legal framework. You don’t need to be the best, you just need to be better.

Kalshi won.

The CFTC lost–at least on paper.

But the real loser?

As is often the case, the American public.

That may sound populist, but if you look through a fairness lens, it becomes clear that it’s simple math, not politics. If a statute is designed to protect the public, and the agency abandons the interpretation that actually serves that purpose, the public inevitably loses.

What If…

The CFTC would have adopted Approach #1?

If the CFTC had fought the public-interest fight, they may still have lost. To see why, it is helpful to think of the public interest determination as a spectrum (PDF, Page 13) with entertainment at one end and economic purpose at the other.

Will President Trump say “six seven” during the State of the Union? That contract doesn’t do anything economically useful for anyone, and is best described as: Frivolous.

What about event contracts on inflation, or interest rates? Those sit toward the other end of the public-interest spectrum.5 Sure, some will still use it for pure speculation, but there is arguably enough of a constituency that uses it for genuine risk hedging. On balance, it’s reasonable to conclude that these contracts matter to the functioning of the economy and therefore serve the public interest.

Election markets sit at an awkward middle ground. They aren’t essential like interest rate or inflation contracts, but they aren’t frivolous either. In a previous post, we described this middle ground as recreational–just purposeful enough that you can make a credible argument for them, but not clearly align with the public-interest bar the statute envisions. Twice in history, the CFTC concluded they didn’t meet that bar. Had the agency maintained that position, the Court might have agreed. Or, it might have found just enough public interest to let them through.

What actually happened (Approach #1.5): Kalshi won. Election contracts were allowed.

What could have happened (Approach #1): Kalshi might still have won. Election contracts might still have been allowed.

To a casual observer, these outcomes may look the same. The scoreboard records a win for Kalshi under either scenario and election contracts are good to go.

But from a legal precedent and regulatory evolution perspective, there is a big difference between the two. Under the former scenario (what actually happened), the public-interest framework is dismantled. Under the latter (what could have happened), the public-interest framework would have remained intact. But, under the latter, the post-litigation world would have looked very different:

The CFTC would have lost the battle but won the war–and the American public would have won with them.

Frivolous, Recreational or Essential? The CFTC's Missed Opportunity

Last week, we continued our coverage of the Kalshi v. CFTC case. We explained how The Court of Appeals for the D.C. Circuit saw through the ambiguity but the CFTC missed its moment.

There was a little hope though because the CFTC would get a second chance.

Unfortunately, they chose to concede that opportunity.

The CFTC Gets a Second Bite at the Apple

The general consensus in this universe is that most people get a second chance. They should. Mistakes happen. Wrong turns happen. People fall off the wagon. Life can be forgiving–or at least tries to be.

The judicial system seems to reflect this as well. You may not raise new issues on appeal, but you can argue differently. You can correct course and have another bite at the proverbial apple.

Historically, the government gets even more leeway.

For a moment during oral argument, it looked like the CFTC might seize that opportunity. Rob Schwartz opened with:

To build and maintain a thriving derivatives industry that is distinct from the gambling business has been the work of 175 years, and it’s important.

He later joked on X that his opening was a real banger. Beneath the humor was an unspoken truth: This is the heart of the prediction markets debate.

Was the CFTC about to reestablish itself as the beat cop?

Was the CFTC about to return to Approach #1?

No. They weren’t.

The Court of Appeals seemed puzzled–even frustrated. Not because “gaming” might mean “gambling,” but because the CFTC wasn’t arguing for that interpretation. The judges practically nudged them toward it, like a teacher guiding a student to the right answer.

The CFTC refused to change course, though.

The Court had the authority to reject both sides’ interpretations—a possibility that was either a glimmer of hope or a terrifying prospect for the CFTC, depending on their vantage point.

Defining Success

Did the CFTC truly believe they would lose?

Former acting chair, Caroline Pham, thought so (see the 37:56 mark).

I disagree.

I believe there was a 70-80% chance the Court of Appeals would have reversed, or at least remanded—instructing the district court to resolve the case on public-interest grounds using the economic-purpose test.

Kalshi might still have won.

But they would have won the right way.

The CFTC would have lost the battle but won the war.

So let’s ask the consulting question:

What does success look like?

If success meant preventing election markets from reaching consumers, the path was obvious:

Wait for the appeals result;

Petition SCOTUS if necessary;

Initiate review of Kalshi’s new self-certified products; or

Initiate review on other prediction-market products.

None of that happened.

If a high-school senior insists college is the top priority but never studies, never takes the SAT and never applies, do we take them seriously?

So maybe the agency’s definition of success was something other-worldly.

Could losing the Kalshi fight have actually been the “win”?

Cynical? Maybe.

But let’s trace the steps:

Dismiss the appeal - you can’t afford a remand, let alone a reversal;

Don’t initiate a review if contracts that are likely contrary to public interest are self-certified;

Decline to conclude reviews already initiated; and

Withdraw legacy rulemakings that might constrain future flexibility.

These are the steps that actually did happen; all of them.

Define success one way and none of the expected actions occurred.

Define success another way and every expected action occurred.

Which definition seems more plausible?

We don't have to guess blindly. There is a smoking gun:

The “Obstacles”

Between declining the invitation by the Court of Appeals to argue broadly (January 2025) and choosing to dismiss the case in its entirety (May 2025), the CFTC described its own historical positions–and Kalshi’s–as:

Key obstacles to balanced regulation of prediction markets.

Among the “obstacles”8:

Prior Commission orders issued to designated contract markets (DCMs) pursuant to regulation 40.11 and related Commission interpretations;

Event contract rulemakings;

Federal court opinions, including that “gaming involves games”;

The CFTC’s legal arguments and litigating positions;

CFTC-registered entities’ legal arguments that sports event contracts constitute “gaming” and are therefore prohibited under the Commodity Exchange Act;

Staff interpretations, other guidance, and current practices on event contracts;

Existing law and regulation applicable to DCMs and futures commission merchants (FCMs);

CFTC examinations, enforcement actions and investigations;

Constitutional considerations; and

Federalism, tribal sovereignty and state-regulatory issues.

These weren’t obstacles.

They were the legal landscape.

Calling them obstacles screams “arbitrary and capricious.”

The roundtable that was supposed to address them?

The CFTC canceled it without providing any clarity around the decision. We know because we attempted to participate in the process.

The Train Moves On–and a New Character Boards

Had the CFTC adopted Approach #1, we wouldn’t be here discussing how Kalshi and Polymarket are eyeing $20 billion valuations. Election markets might have survived, but the platforms would have looked more like Iowa Electronic Markets without the cap–not financial behemoths oscillating between media darling and villain.

States wouldn’t be litigating preemption.

There would be no litigation sequencing.

The train would have already reached its final destination.

The last “obstacle” was a potential court order restoring the economic purpose test and reversing (or remanding) the case on those grounds.

On May 5, 2025, the CFTC removed itself from the permissibility fight for good. Tarek Mansour celebrated. Prediction markets had the “right to exist”:

Stop #1 was complete.

The engine was running.

The train was leaving the station.

Just as the conductor announced “doors closing,” someone in a UCLA hoodie sprinted through the narrowing gap:

May 5, 2025 wasn’t just the day the CFTC dropped its appeal. It was also the day PwC dropped me–after 19 years, three offices and two countries.

One door closed.

Another opened–just enough, and not for long.

The message from the universe was clear:

Hop on the train. It’s about time.

The Brookings Institution deregulation tracker: https://www.brookings.edu/interactives/tracking-deregulation-in-the-trump-era

CFTC’s ‘Top Cop’ Legal Team Eliminated Amid Embrace of Crypto, Prediction Markets:

https://finance.yahoo.com/news/cftcs-top-cop-legal-team-161236038.html

“[T]he statute is unconstitutional, and, arguendo, even if it were constitutional, the regulation would still be invalid.”

“For the dozen or so members of the DMO’s product review team, event contracts raised novel questions. Under the Commodity Exchange Act, the regulators could block contracts tied to gaming that weren’t in the public interest, but no one had taken the time to define what gaming actually was. Beyond that, it was unclear whether the CFTC had a right to consider whether a contract was in the public interest or if the agency had an obligation to do so in every case. And how was it supposed to decide what was in the public interest anyway? ‘To be honest, the whole thing was a mess,’ another person with direct knowledge of the CFTC review says. The agency declined to comment for this story.” (emphasis added)

Figure 2 in our Comment Letter: https://www.lexiconlabs.com/_files/ugd/8497cc_a435cea9dc9949b8b3097a99ee21b9fb.pdf

Shortened/edited slightly to improve flow. See originals here: https://www.cftc.gov/PressRoom/PressReleases/9046-25