Predicting The State of the Union

When Speech Becomes Tradeable

“He shall from time to time give to the Congress information of the state of the union, so people can bet on it.”

Says Article II, Section 3 of the U.S. Constitution, not!

The Constitution requires only this: That the President “from time to time give to the Congress Information of the State of the Union...” That’s Article II, Section 3. A duty to inform. A duty to recommend. Not a prime-time spectacle. Not a meme laboratory. And certainly not a tradable asset.

Yet today, the constitutional obligation to report to Congress has become a nationally televised ritual–and now, a prediction market on whether specific words will be spoken. The distance between “information to Congress” and “Yes 11% / No 90%” is the distance between constitutional design and nationwide gambling.

So what will President Trump say during the State of the Union? Supreme Court?

It makes sense, right? The Supreme Court just ruled Trump’s tariffs are illegal. Justice Gorsuch’s concurrence in particular received much attention, with Professor Bainbridge accurately depicting it as him “spanking colleagues to his left and his right.” Trump didn’t like the decision. He immediately imposed an import duty of 10%, then just one day later upped the ante again and made it 15%.

For the opportunist with conviction, this is as close it gets to “free money.” As of Sunday morning, the contract could be had at 87 cents–meaning if President Trump utters those two words, that’s an almost 15% return in just two days. In 2025, you had to wait close to a year for the S&P 500 to return that and that was a good year. Why not “invest” in prediction markets (LexBeyond podcast Ep. 13)?1

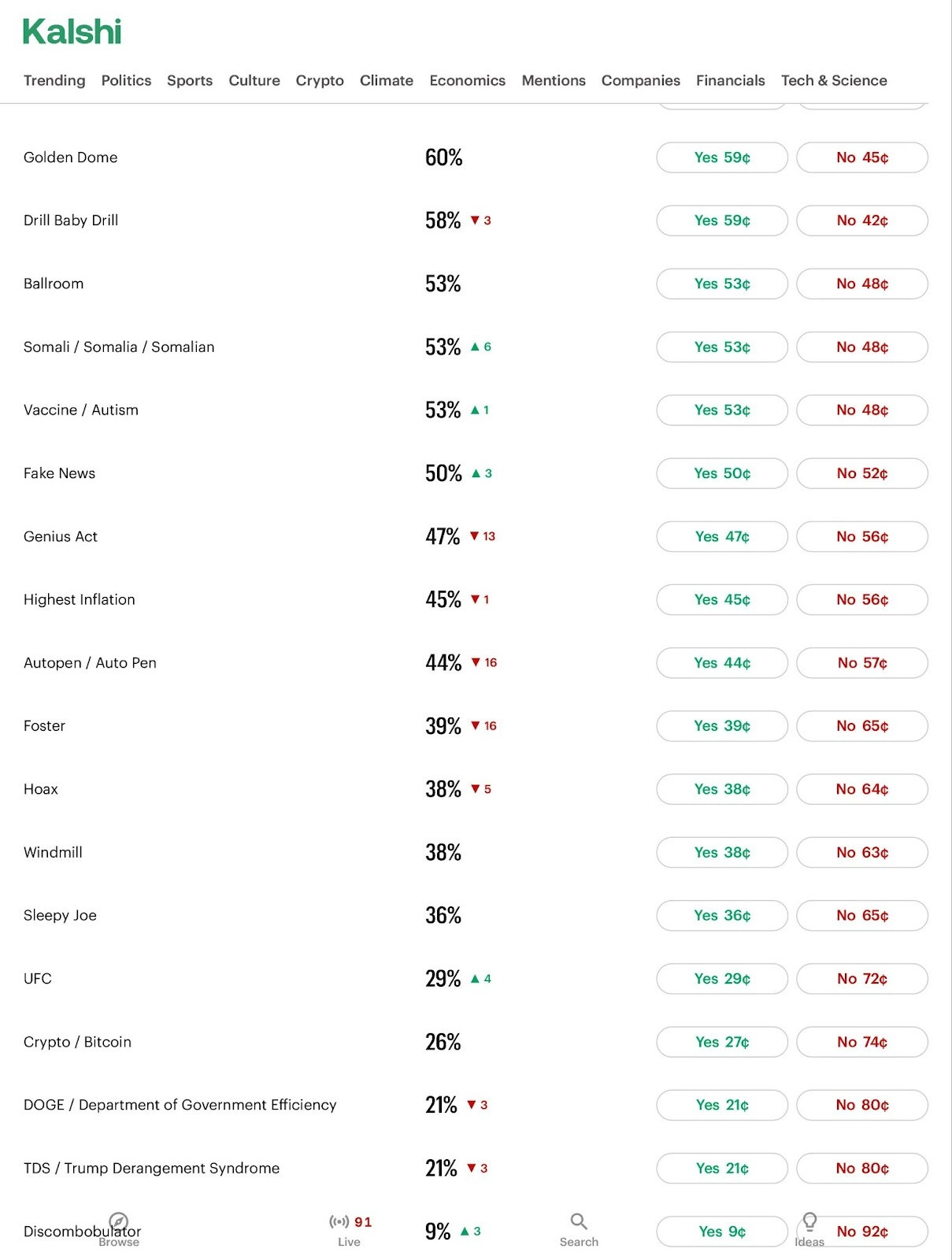

And if you want to get ahead even faster –whether because you’re a reckless gambler chasing a Lambo or a disillusioned Gen Z who’s lost trust in America– the menu gets even more absurd. Sunday morning offered these:

Genius Act was at 47%, but traders were losing hope. Maybe Brian Armstrong is too optimistic?

Sleepy Joe at 36%. Yes: A financial instrument on whether the current POTUS will call out the former POTUS during the SOTU. Mockery is in prediction markets’ DNA, so why not?

Crypto/Bitcoin at 26%. If Bitcoin isn’t moving, why bother with the token when you can bet on the mention instead?–a potential 4x payout in just two days.

And if you want even more meme-level material to gamble on, don’t fret. There’s a market for that, too.

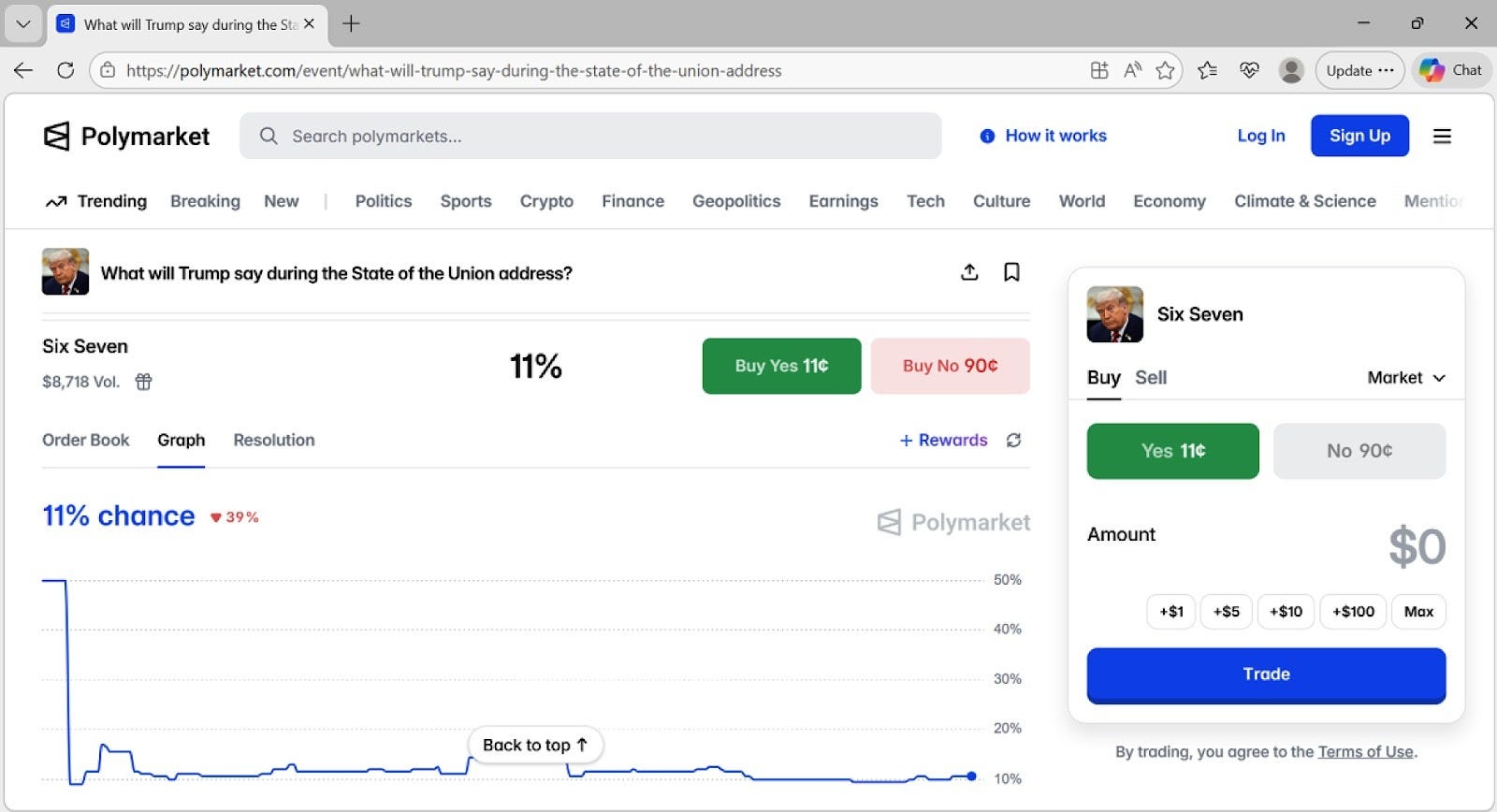

Will the President Say Six Seven During the State of the Union Address?

It’s more likely than not that you’ve heard “six seven” in recent times, but just in case you haven’t, this is the video that started it all:

It’s hard to believe that this was only a few months ago. It feels longer. My kids are telling me that the meme has already passed. Maybe. But it’s still culturally relevant enough to make it into SOTU trading markets. And while this commenter captured the ridiculousness of the meme…

…the real irreversible damage won’t come from the millions of kids joking around. It will come from those same kids having the ability to wager on whether the President of the United States will say “six seven” during the State of the Union address.

Article II, Section 3 requires the President to provide Congress with information. That is the constitutional architecture. What it does not require is a broadcast spectacle priced in real time–with odds attached to syllables. When we move from “information of the State of the Union” to pricing whether the President will say “six seven,” we are no longer debating policy. We are commodifying rhetoric.

It’s hard to imagine that’s what the Founding Fathers had in mind. So, just short of our beloved country’s 250th birthday, how did we get here?

If you’re a reporter covering prediction markets, a lawyer tracking nearly 40 cases, or simply a spectator wondering how all of this happened, we can offer some insight. We didn’t sit down one weekend and do superficial research. We’ve been at the center of this (albeit not always visibly), for the last 25 years.

2000 - When The Rope Comes Down

It started at the turn of the century.

The markets were humming. The dot-com bubble hadn’t burst yet. This time was truly different. The future was undervalued, according to Wired, which boasted that its WIRX index (a group of 40 companies “leading the transformation of the economy”) delivered an 81% return. It was a mixed bag: Microsoft and Amazon... but also Enron and WorldCom.

So, no, this time was not different, but the perception was that it was. And perception drives legislation. The result? The Commodity Futures Modernization Act (“CFMA”) of 2000.

It was a strange response. Brooksley Born, CFTC Chair from August 1996 to June 1999, had been genuinely worried that off-exchange trading would be the industry’s Achilles’ heel. She lacked visibility and didn’t like it. One of the few remaining responsible adults in the room, she took the challenge head-on. This Frontline documentary is a must watch:

Her warnings alienated the powerful trio of Federal Reserve chairman Alan Greenspan, Secretary of the Treasury Robert Rubin, and Deputy Treasury Secretary Larry Summers. Arthur Levitt, SEC Chair at the time, was also in that camp.

Born wasn’t one to give up easily. When Genius Failed, it briefly seemed like her warning signs might be heeded. But Greenspan charmed Congress, calling Long Term Capital Management’s collapse an anomaly. Just like the 1907 panic (LexBeyond podcast Ep. 15), it was a “rare occasion.”

The writing was on the wall. Nothing protective would be done about OTC derivatives markets. Born resigned. The Working Group, led by Paul Architzel on the CFTC side, went to work. One of its key findings (PDF):

A cloud of legal uncertainty has hung over the OTC derivatives markets in the United States in recent years, which, if not addressed, could discourage innovation and growth of these important markets and damage U.S. leadership in these arenas by driving transactions off-shore.2

When the storm passed, Congress inexplicably doubled down, enacting the CFMA.

The CFMA did three things–a lethal combination:

Removal of the approval process. That was the velvet rope that came down. Previously, the CFTC had to approve all products. After the CFMA, they approve only if exchanges specifically ask for it (almost no one does). Instead, exchanges can just self-certify and are trusted to self-regulate.

Repeal of the economic purpose test. Futures markets were for hedging and price discovery and the economic purpose test was the mechanism to separate economically useful futures from gambling. Through the CFMA, Congress instead opted for vague language about “financial, commercial or economic consequence.”3 The CFTC lost its formal grading authority.

Off-exchange trading legitimized. The CFMA created regulatory tiers allowing institutional actors to transact in largely unregulated OTC swap markets.

In other words, Congress gathered the wood, lit the fire, and then poured gasoline on it.

To many, 2008 was a black swan event. To those tracking the law in real time, it was entirely predictable. As the late Lynn Stout described so eloquently:

In other words, the credit crisis was not primarily due to “innovations” in the markets or the legal system’s failure to “keep pace” with finance. The crisis was caused, first and foremost, by changes in the law. In particular, the crisis was the direct, foreseeable, and in fact foreseen (by the author and others) consequence of the CFMA’s sudden and wholesale removal of centuries-old legal constraints on speculative trading in over-the-counter (OTC) derivatives.

Brooksley Born was proven right. Arthur Levitt would eventually apologize:

I’ve come to know her as one of the most capable, dedicated, intelligent, and committed public servants… I wish I knew her better in Washington. I could have done much better. I could have made a difference.

Too little too late.

2008 - When America Feels The Pain

The 2008 recession was the worst crisis since 1929. Congress responded with Dodd Frank–not streamlining, as Kalshi argued, but for cleanup. Reform was literally in the name.

If the CFMA brought America to its knees in three steps, Dodd-Frank walked back one and a half:

Off-exchange trading restricted. Off-exchange trading has always been disfavored. It just so happens that America has to go through cycles to remember that core principle. The first time it happened was when the bucket shops were the original financial grift (LexBeyond podcast Ep. 14). SCOTUS intervened (PDF) and crippled them, but it took a panic to finish the job. The same happened with the 2000 deregulatory wave, but the 2008 recession was what triggered the Dodd-Frank reform.

America just needed to see the pain for Congress to bring swaps into the regulatory perimeter. Did that prevent all swaps from trading off-exchange? No. Refer to our sports gambling coverage in Tennessee (LexBeyond podcast Ep. 16). Orange is the new black.Economic purpose restored. Somewhat. It returned in the context of event contracts. Congress was aware of the prediction markets trading in death, so terrorism, assassination and war were explicitly called out in the special rule. And since incentivizing an unlawful act through event markets trading is a bad idea in general, that principle was codified into law as well. But there were a ton of futures on other commodities, sports being the main one, that would serve no economic purpose, so the “gaming” prong rounded out the list to “to restore CFTC’s authority to prevent trading that is contrary to the public interest.” (Congress’s words).

Event markets aren’t new–they predate America (LexBeyond podcast Ep. 12). The insurable interest doctrine exists (you can insure your health but not mine) because 18th-century England learned the hard way that betting on strangers’ lives was a terrible idea. America had to go through a similar experience to reach a similar conclusion.Self-certification untouched. The rope remained on the ground. Anyone with a license could list anything. The beat cop had to kick out what didn’t belong. What could possibly go wrong?

2024 - When The Cop Goes Off-Duty

If you’re wondering why the “six seven” market exists–or why sports gambling exploded nationally–you must understand what Dodd-Frank did. It gave the CFTC discretion to separate genuine futures trading from gambling through the special rule.

We mentioned Paul Architzel earlier. He comes up in this blog not just because he helped architect the CFMA, but because he also served as our external counsel for years as we navigated the CFTC’s regulatory maze around our own products.

A surface-level read of history makes it easy to cast Paul as the villain–the guy who designed the blueprint for a mess. This view is too convenient though. Knowing the man, and having worked with him closely, it’s clear the problem wasn’t malice or an invitation to the Wild Wild West. It was something more ordinary, and in some ways more dangerous: He assumed people and institutions would behave better than they actually do. He believed market participants would self-regulate. He believed the CFTC would stay principled enough to police the boundaries. He believed the equilibrium would hold.

It didn’t.

Former Commissioner Quintenz commented regarding the axing of the economic purpose test:

In 2000, the CFMA repealed Section 5(g) of the CEA in its entirety. Exchanges no longer had to affirmatively demonstrate a public interest for their contracts by meeting an economic purpose test for their contracts’ hedging utility.

Yet when Paul advised us–before Dodd-Frank–he didn’t say, “Economic purpose is gone, self-certify whatever you want.” Instead, he urged us to develop contracts that “would have met the old ‘economic purpose test.’” That was the CFTC’s North Star, repealed or not.

In 2024, the CFTC turned its back to its North Star and shortly thereafter lost its case against Kalshi. The Court of Appeals briefly looked like it might save them. Perhaps that scared the agency, because it threw in the towel before a decision was rendered.

Surprising? Not really. Months earlier, the CFTC described its own litigation positions, court opinions, proposed rulemaking and even Kalshi’s position on sports event contracts as:

“Obstacles.”

That word was the tell.

Almost a year ago to the day, we couldn’t help but wonder:

Has the CFTC already decided that they will regulate prediction markets, including sports-related event contracts, and these things stand in the way?

Twenty three Senators now seem genuinely surprised (PDF) that Chair Selig told Congress one thing and is doing another. Surprise is the failure of expectation. The signs were there. If the CFTC truly didn’t know what to do with sports event contracts, it certainly wouldn’t have described its litigation positions, court opinions, proposed rulemaking and even Kalshi’s position as obstacles. Apparently, that’s what the minimum effective dose of regulation means–if you don’t like the position the entity you regulate took, one you agreed with no less, get it out of the way, whatever it takes.

Paul once told us (in the context of sports):

I doubt that the CFTC would ever find a contract acceptable that relies on specific-performance related outcomes.

We believe Paul’s mistake was twofold:

He believed market participants were as principled as he was; and

He believed the CFTC would remain principled enough to stop them if they weren’t.

He assumed an equilibrium of trust. But when the letter of the law disappears, the spirit survives only as long as principled adults remain in the room.

Eventually they don’t.

The revolving door accelerates the decline:

The responsible regulators get crowded out. The CFTC becomes an advocacy center for prediction markets.

Justice Gorsuch captured the danger in Learning Resources (the recent tariff case) (PDF):

Our founders understood that men are not angels, and we disregard that insight at our peril when we allow the few (or the one) to aggrandize their power based on loose or uncertain authority. We delude ourselves, too, if we think that power will accumulate safely and only in the hands of dispassionate “people . . . found in agencies.” Even if unelected agency officials were uniquely immune to the desire for more power (an unserious assumption), they report to elected Presidents who can claim no such modesty. (internal citations omitted).

We believe Paul had the country’s best interests at heart, but he likely deluded himself.

A Possible Path

Despite the chaos, prediction markets’ confidence isn’t misplaced. Federal preemption is real, but it’s only one part of the three-legged stool. The true debate: Preemption + permissibility + off-exchange trading, and that’s what we believe the SCOTUS will address. If SCOTUS resolves only the narrow preemption question, prediction markets will win.

In that latter scenario, the “six seven” market becomes expressly legal within a couple of years. The current view seems to be that it’s already legal on the federal level. But if SCOTUS stamps it?

All bets are on (pun intended).

Which tweet will go viral?

Is Joe next door cheating on his wife with Susie?

Will little Jack be bullied in school this week?

And of course, the grand prize: Sports.

Along with every imaginable bet that, at best, does nothing for America–and at worst, brings out the absolute worst in humankind, every State of the Union would turn into a gambling bonanza.

Just like the Founding Fathers drew it up.

At the time of press, the price was down to 76 cents.

The U.S. vs. offshore story would of course be familiar to anyone who is watching what is happening today in regulatory circles.

It is not entirely clear whether this language was meant as a substitute for the economic purpose test (if so, it did a poor job), or clarification of expansive CFTC jurisdiction. Subsequent legislation (Dodd-Frank) and the word choices Congress made therein strongly suggests it is the latter.