The Redacted Middle

Massachusetts and Tennessee have put prediction markets, sports betting and the CEA on a SCOTUS collision course

When Judge Barry-Smith released his opinion in Massachusetts a few weeks ago, the scoreboard moved to 5-1. State-rights advocates rejoiced. Tribal regulators were pleased. The emerging narrative was simple: Prediction market litigation was becoming a nightmare for Kalshi.

Then, a month later, Judge Trauger issued her decision (PDF) in Tennessee–and this time Kalshi walked away with the win. Suddenly, it was the prediction markets’ turn to celebrate.

But, the real story isn’t that Kalshi lost in Massachusetts and won in Tennessee. With dozens of cases in motion, both wins and losses are expected. At this point, this whole thing resembles a basketball game: States on one side, prediction markets on the other, trading baskets back and forth.

The real story is that both judges–despite reaching opposite outcomes–effectively agreed on a foundation consisting of three closely connected statements. Once you follow that shared premise though to its logical conclusion, you arrive somewhere deeply inconvenient:

State-regulated sports betting may be nearing its end.

Massachusetts: The Silence that Matters

Judge Barry-Smith issued his opinion on January 20:

In an earlier podcast, we argued that Kalshi may “out-Brady” Massachusetts–not because Kalshi won (they didn’t), but because the opinion unintentionally exposed a structural vulnerability in state-regulated sports betting:

The core problem? An extremely consequential act of silence sandwiched between two correct conclusions.

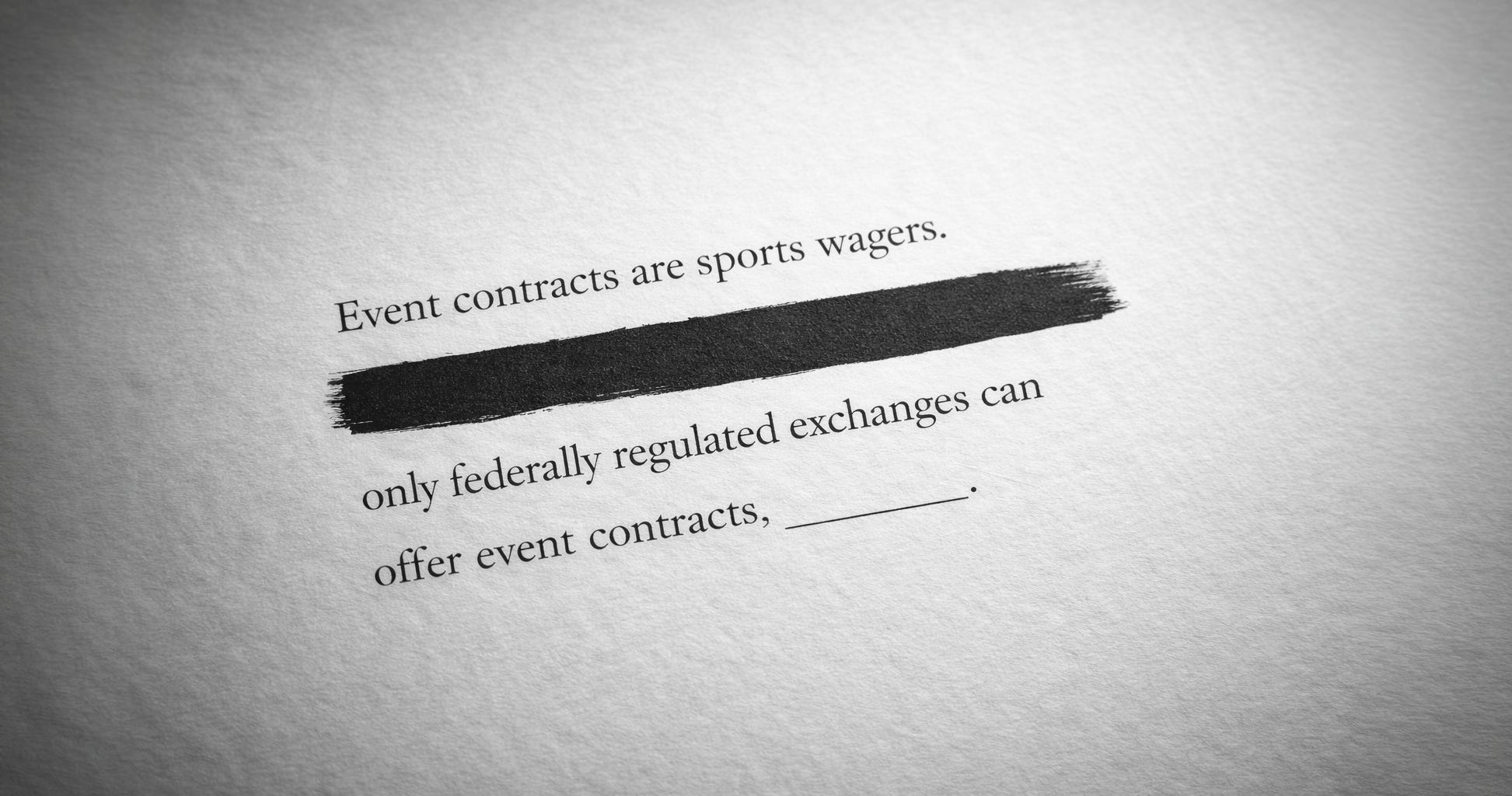

Conclusion #1: Event contracts are sports wagers.✅

Judge Barry-Smith states:

The defendant… operates a nationwide ‘prediction’ market… on which traders can purchase… ‘event contracts,’ including the outcome of sporting events.

And:

Kalshi does not argue that its sports-related event contracts do not meet the definition of sports wagering in the Commonwealth.

Easy enough.

Conclusion #2: Only federally regulated exchanges can offer event contracts. ✅

Judge Barry-Smith observes:

Under the CEA, only federally regulated exchanges can offer event contracts.

No objections, Your Honor. That is the law.

Here is our question regarding the inverse proposition:

If event contracts are sports wagers… are sports wagers event contracts?

Silence.

Judge Barry-Smith failed to recognize or chose to remain silent on what truly matters:

That silence–the “redacted middle”–is the only thing standing between state-regulated sportsbooks and a federal prohibition.

With that executive summary in hand, let’s work through the details.

Judge Barry-Smith clearly identifies Kalshi as an event-contract platform:

Kalshi launched its platform in 2021, with event contracts focused on topics including inflation, the consumer price index, unemployment and macroeconomic benchmarks.

In January 2025, Kalshi began offering sports-related event contracts.

So the question becomes unavoidable:

Who is legally allowed to offer event contracts?

Judge Barry-Smith answers unequivocally:

Under the CEA, only federally regulated exchanges can offer event contracts. 7 U.S.C. § 2(e). (emphasis added)

There is one issue with how he frames the statute: While the CEA does use the phrase “event contracts,” the specific provision he cites, § 2(e), does not, and instead speaks only in terms of swaps.

Is that a problem? Not necessarily. If event contracts are swaps, then his bottom-line conclusion still holds.

But here is another loose end, which eventually leads to an existential problem for state-regulated sportsbooks: Judge Barry-Smith “assume[s] without deciding that Kalshi’s event contracts are swaps.”

→ Swaps can only trade on federally regulated exchanges - yes.1

→ The cited statute, § 2(e), does not mention event contracts, but the opinion implies that.

→ That’s not an issue if event contracts are swaps, but…

→ The opinion is silent on whether event contracts are swaps.

This doesn’t exactly hold together, does it? It feels… incomplete. For the critical reader, the opinion results in more questions than answers and it leaves the door wide open:

How should we characterize sports wagers?

Are sports wagers event contracts?

Are sports wagers swaps?

If yes to either, what does that mean for DraftKings and every other state-regulated sportsbook?

The answers are rather straightforward (but you won’t find them in the opinion):

Yes.

Yes.

It means state-regulated sportsbooks are engaging in unlawful activity, strictly prohibited by the CEA.

That’s the existential threat hiding inside the Massachusetts opinion.

Precision matters here. When a judicial opinion invokes “event contracts” and immediately cites a statutory provision, readers naturally assume the statute contains that term–especially in a case where the entire dispute turns on what an event contract is and who has jurisdiction. With nearly forty related cases moving in parallel, every court is watching every other court. In that environment, even small linguistic choices carry outsized weight.

Tennessee: Revealing the Redacted Middle

The Tennessee decision goes even further–it doesn’t just echo Massachusetts (different conclusions, yet the same reasoning); it highlights the existential threat facing state-licensed sportsbooks even more strongly. In our recent podcast, When the Duck Meets the Mockingbird, Lex & Bianca walk through that reasoning in less than five minutes:

That said, let us memorialize the logic here as well. Judge Trauger has no trouble reaching the exact same conclusions as Judge Barry-Smith:

Conclusion #1: Event contracts are sports wagers. ✅

From the opinion:

In other respects, it does resemble traditional sports betting. As the defendants argue, Kalshi has marketed itself as a traditional sports betting operation.

Indeed.

Conclusion #2: Only federally regulated exchanges can offer event contracts. ✅

Judge Trauger observes:

Under the CEA, only exchanges regulated by the CFTC—known as designated contract markets (“DCMs”)—can offer event contracts. (emphasis added)

Once again, no objections, Your Honor.

But where Massachusetts stayed silent, Tennessee takes a half-step further, which leads to a reveal of the “redacted middle”:

And, based on Kalshi’s description of its operations, although there may be differences under the hood between trading on Kalshi and placing a bet with a licensed sportsbook, for any sports-betting enthusiast unfamiliar with the CEA, it appears to the court that a user would find Kalshi’s offerings similar, if not identical, to a sportsbook. (emphasis added)

In other words, the court says Kalshi’s offerings appear “similar, if not identical” to a sportsbook. And “identical,” as Merriam-Webster reminds us, means:

Being the same, or

Having such close resemblance as to be essentially the same.

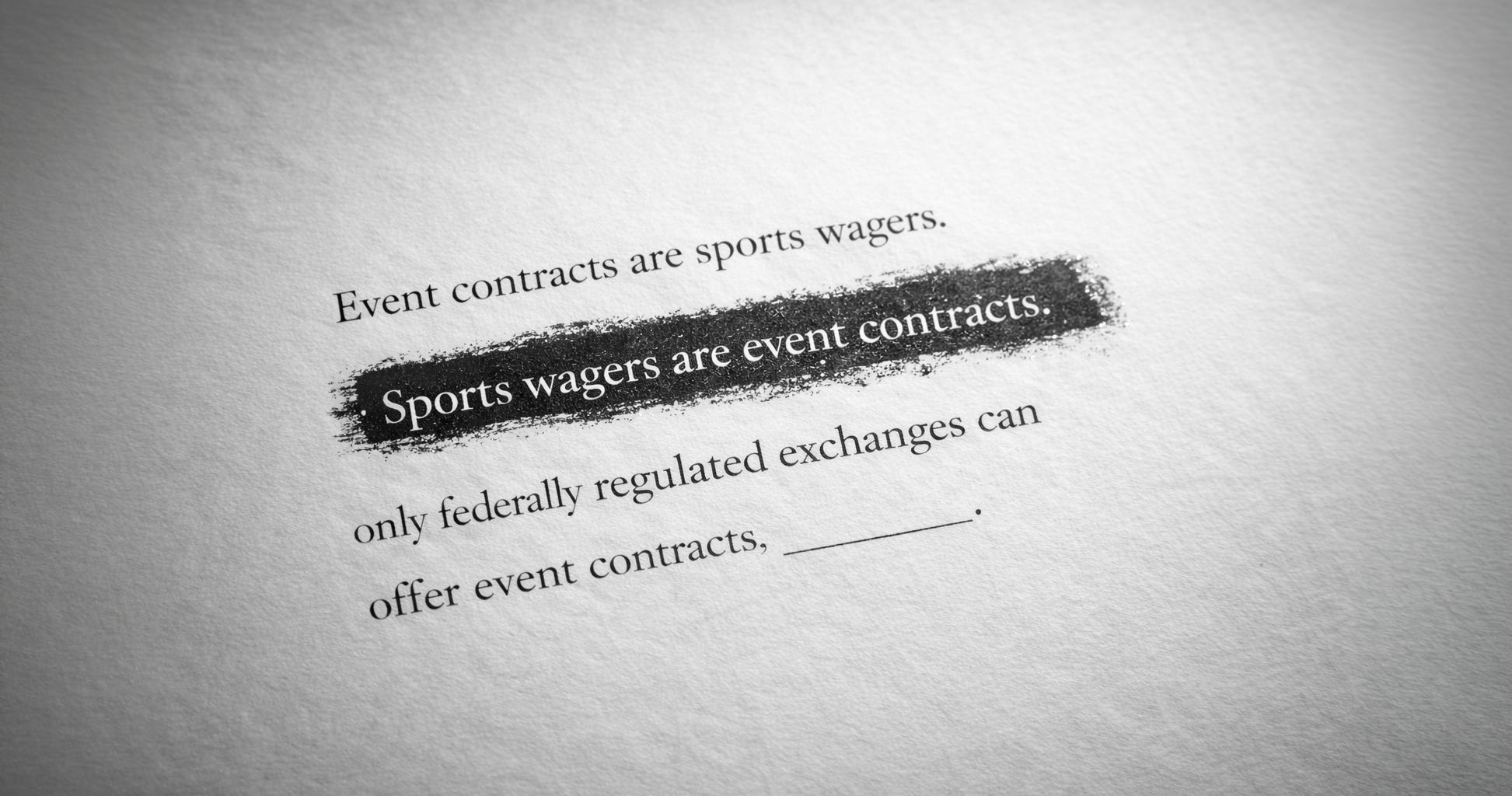

If A is identical to B, then B is identical to A.

If sports event-contract trading is identical to sports betting, then sports betting is identical to sports event-contract trading.

Which then, logically, means:

Sports wagers are event contracts.

Of course the decision doesn’t reveal this in a quotable line—but it delivers it unmistakably in substance.

That is the “redacted middle”–revealed.

Once you accept that equivalence, the rest follows in line automatically, allowing us to fill in the blanks to complete the picture above.

Event contracts are sports wagers;

Sports wagers are event contracts; and

Only federally regulated exchanges can offer event contracts.

Therefore, state-regulated sportsbooks are offering event contracts in violation of a federal statute.

Technically speaking, there are some exemptions provided by the statute, but it is extremely unlikely that sports event contracts can claim them.