What Paul Grewal Gets Right About Prediction Markets—and What Comes Next

Litigation sequencing, unanswered questions and SCOTUS predictions

Thoughtful Q&A by Nick Devor with Paul Grewal raises exactly the right questions about jurisdiction and the future of prediction markets. Grewal’s answers follow a familiar, and revealing, pattern: Confidence on preemption, caution on permissibility and calibration on parallelism.

That structure is not incidental. It reflects where Coinbase’s chief legal strategist knows he is strongest, where he knows he is weakest and where he is playing the long game.

Let’s break it down:

Grewal’s Confidence On Preemption

Grewal oozes confidence on preemption, and for good reason. Yes, the scoreboard today appears lopsided in favor of the states (Currently 13-21):

But, Grewal doesn’t seem bothered—and his confidence is not misplaced.

He knows the law is on his side, and it’s not a close call.

The states’ Achilles’ heel has always been the same: Their theory has no limiting principle, and courts generally do not endorse positions that have no logical stopping point. For a while, states tried to keep the fight contained to sports. That doesn’t mean they would be able to produce a coherent answer when they face the more difficult question: If you can regulate sports event contracts, can you also regulate election contracts?

A natural tension emerges here. Once a state asserts authority over one category of federally regulated event contracts, it becomes more difficult to articulate why that authority wouldn’t extend to others. Even if a state wanted to draw a boundary, it’s not obvious where that boundary would come from or how it would be justified under the structure of the Commodity Exchange Act. That uncertainty is what keeps the limiting principle problem alive.

That uncertainty could, in theory, hide behind a shield if the states only challenged sports event contracts. They aren’t, so that rhetorical shield is now gone.

Nevada’s recent state-court ruling (PDF) against Coinbase reaches elections. Kalshi was criminally charged in Arizona two weeks ago, and four of the counts are related to election contracts. Minnesota’s bill lumps elections together with sports and other commodities.

The states are no longer cabining anything–they’re reaching for everything. As Grewal himself put it, “... they want it all.”

When states claim jurisdiction over sports, elections and whatever else they can grab, they recreate the exact regulatory chaos Congress worked so hard to prevent with the 1974 Commodity Futures Trading Commission Act. They’re trying to reinvent the wheel that Congress already fixed decades ago.

Grewal knows this and knows how these stories end.

The scoreboard may not reflect it yet, but the momentum has shifted. This feels like one of those games where the team in the lead is beginning to lose control–and everyone watching can feel the start of the comeback (If you remember the Falcons vs. Patriots Super Bowl you know what I mean).

Grewal’s Caution On Permissibility

“Not every silence is pregnant,” the Supreme Court once said (quoting another case).

But this one is.

Grewal knows his strongest argument is preemption.

He also knows his weakest argument is permissibility.

So when Barron’s asks the most obvious question:

Prediction markets ask users to put money on the likelihood of future outcomes. Is that not gambling?

Grewal disregards the gambling notion and immediately pivots back to preemption. His first sentence:

Prediction markets are a type of derivative contract and derivatives have been regulated by the federal government going on many, many decades now.

I don’t believe anyone can disagree with that response because it’s the truth. His last sentence reinforces his position:

[T]he words of the CEA are very clear: Event contracts of all types, including those related to sports, are derivatives, and therefore not subject to state gaming laws.

Both sentences are true. Both are also safe. Sandwiched between those two bookends he offers a historical aside about how “gambling” has been used to describe futures contracts for a century:

“Gambling” is a term that has been used to characterize certain futures contracts going back to the origins of the CEA. For example, labeling futures contracts on grain as gambling. So while we certainly understand there is a common regular usage of the term in everyday conversation, in the law, words matter.

This is also true and safe.

But notice what he does not do:

He does not address what “gaming” means under the CEA. He does point out (correctly) that this is the CFTC’s call to make, but doesn’t truly elaborate on what he thinks the call should be.

He does not reveal the fact that the only appellate court that has recently analyzed the statute through a gambling/public interest lens, the Court of Appeals for the D.C. Circuit, seemed poised to conclude that “gaming” may be problematic for elections–let alone sports.

We recounted that story in a previous post:

The bottom line is simple and Grewal probably senses this too:

The position that sports event contracts are not “gaming” under the CEA is not tenable.

Grewal’s Calibration On Parallelism

When asked what role the states can play, Grewal offered a carefully balanced answer:

The states have an important and ongoing role in regulating gaming writ large. If there is gaming activity outside of CFTC-regulated markets that don’t involve these event contracts, the states absolutely should play a role in overseeing that activity. But when there’s a contract sitting on a CFTC-regulated market, states have no business under the law set by Congress in attempting to restrict it. And where that happens, I think it clearly is an overreach.

This is the standard prediction-market position:

States can regulate sports gambling within their borders, but they cannot reach into CFTC-regulated markets.

The problem?

That’s not the law.

If sports event contracts are swaps, they can only trade on CFTC-regulated exchanges. Multiple courts have said so. A former CFTC Commissioner said the same thing:

Because that’s not the law, prediction markets will inevitably challenge state-regulated sports betting the moment they secure a preemption win:

Prediction markets are playing the long game.

There’s no reason to try to consolidate power now.

Preemption first.

Off-exchange swap trading later.

And states, for the most part, are letting prediction markets dictate the rules.

Why We’re Here: Litigation Sequencing

Whether intentional or not, prediction-market litigation is unfolding in a way that should make Grewal smile. Preemption–their strongest argument–is the only issue courts are seriously engaging with right now. And, to date at least, the states have taken a commanding lead on that front. That said, much of that is just noise.

Grewal can afford to ignore the noise.

The real question is why preemption is the only live issue. We answered that question in a four-part series on litigation sequencing, and if you read it, we are confident that you’ll find at least one idea you haven’t seen anywhere else:

Predictions: Grewal vs. Lexicon

Devor asked Grewal the right question:

What are the odds that they rule in favor of prediction markets?

Grewal didn’t answer that question.

He answered a different one (jurisdiction):

They will rule in favor of the CFTC’s exclusive jurisdiction over prediction markets. I have no doubt in my mind about that.

That’s the key phrase: CFTC’s exclusive jurisdiction.

On that point, he’s right and we agree.

But here’s what’s really happening:

Prediction markets are framing this entire fight as a preemption debate.

They’ll continue to avoid, defer and dodge every question about permissibility.

Because they know what’s at stake:

If SCOTUS takes only the preemption question, then prediction markets win; but

If SCOTUS considers the rest, things may not go so well for them. Even if prediction markets win on preemption, they may lose the battle over whether they have a right to exist.

So, for clarity, let’s separate SCOTUS ultimately taking the case from the questions they will tackle if they take the case.

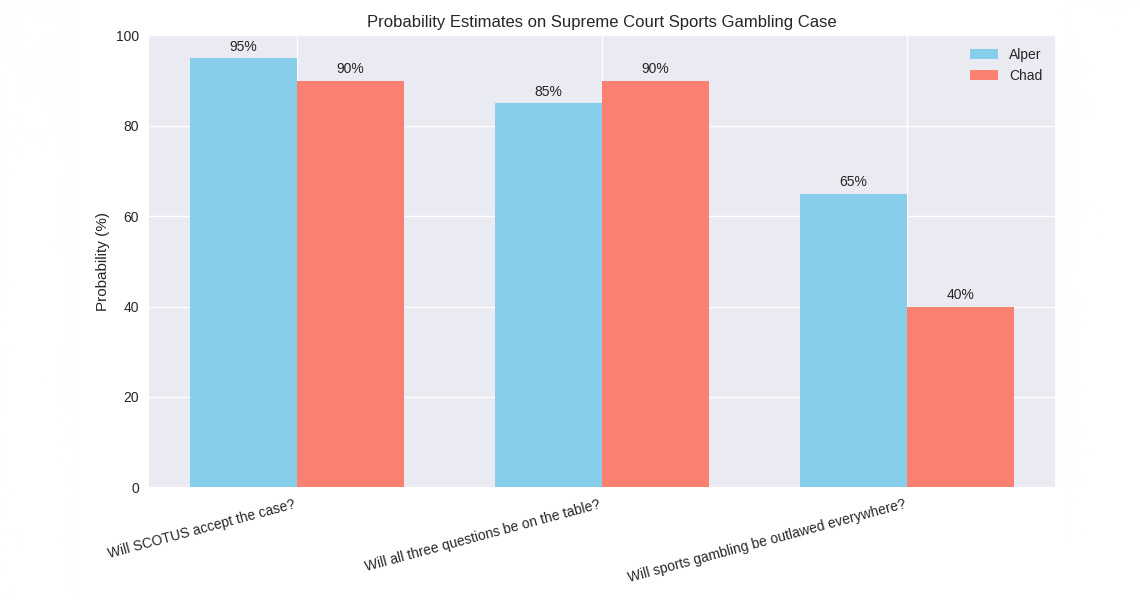

Grewal makes a conservative estimate when asked about the former, stating “the odds are better than 50/50 that the Supreme Court ultimately weighs in.” It’s not clear whether he truly believes that or downplays its significance. We assigned a much higher probability to SCOTUS eventually taking the case than Grewal:

But the second question in the graph above (middle) is the more consequential one. Grewal predicts there is a better than 90% chance that SCOTUS affirms the CFTC’s exclusive jurisdiction. That probability is a conditional one and shouldn’t be viewed as the same estimate as a favorable SCOTUS outcome for prediction markets: It assumes the Court will frame the case around the narrower preemption question. Our prediction is that SCOTUS is unlikely to confine itself to that framing. In other words, the issues currently being litigated in lower courts may not be the full set of questions the Supreme Court ultimately chooses to resolve.

Here are the rest of our predictions and our reasons:

In closing, what do you think will happen? Will it boil down to Grewal’s “nothing-to-see-here” vibes and prediction markets win on preemption or do you assign higher odds, like we did, that SCOTUS will not take the narrower path?

In a quick exchange, Wallach clarified that he is also counting the Coinbase TRO as a win for the states. That ruling came in early February, and the related PI decision is what was issued on March 26, 2026. See Exhibit A (PDF).