The Last Mile, Completed

Carrying John Lothian’s framework to its logical legal conclusion

Last week, we covered the Last Mile Problem In Legal Analysis, the idea that robust legal analysis sometimes stops just short of the conclusion the logic appears to require. Usually, that’s because the conclusion is inconvenient. You walk through a detailed analysis only to discover that your own reasoning leads you somewhere you didn’t want to go:

At that point, the analyst has, broadly speaking, three options:

Option 1 - Acceptance. Inconvenient or not, this is the result; accept it.

Option 2 - Silence. Leave the inconvenient part unsaid. You can sometimes sense this pattern in court opinions.

Option 3 - Denial. Since “absurd” results cannot ensue, go back and change the conclusion.

John Lothian is, literally, a Hall of Famer. Despite that, or perhaps because of it, he can’t bring himself to admit that sports event contracts can be federally-regulated swaps; he ultimately concludes they are not. Today, we’ll walk through his reasoning step‑by‑step, examine where the analysis holds and identify where it breaks. We will be loyal to his nodes of analysis; we will simply repackage his framework and look at it through the Lexicon Lens.

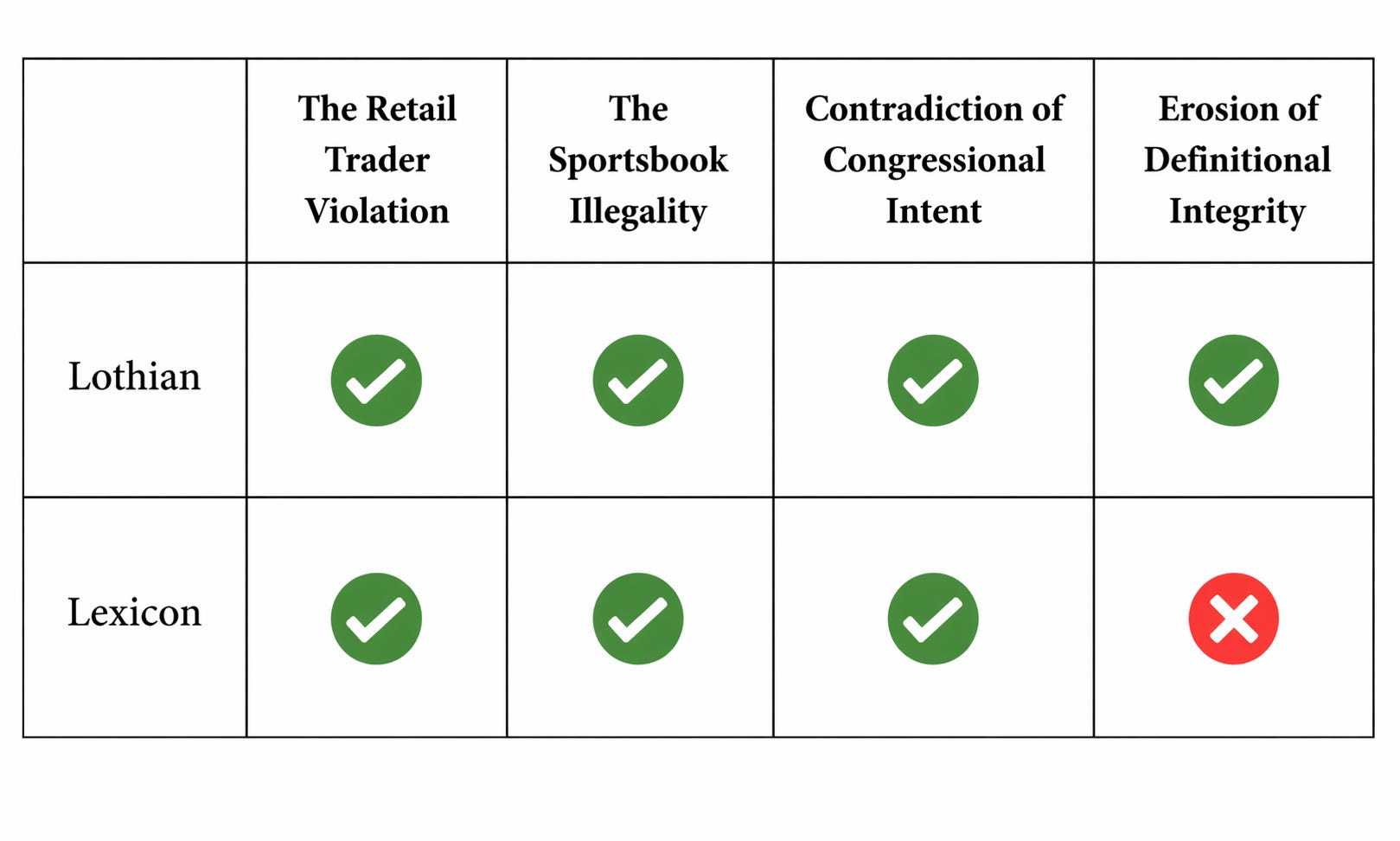

Perhaps the cleanest way to analyze Lothian’s argument is to track his LinkedIn post and, in particular, the comments he made underneath it. Lothian wants to see where the premise that “sports event contracts are swaps” takes him, and his analysis leads him to four conclusions. He is not fond of them–he writes, “The CFTC's broad interpretation of the swap definition creates four key legal and regulatory problems:”

Issue #1 - The Retail Trader Violation (CEA Section 2(e)): If prediction market contracts are classified as swaps, retail participants (who are non-Eligible Contract Participants or non-ECPs) may only legally trade them on a Designated Contract Market (DCM). Trading these products on non-DCM platforms, such as offshore or decentralized exchanges, constitutes a violation of federal law under CEA Section 2(e).

Issue #2 - The Sportsbook Illegality: The same logic implies that the functionally equivalent products offered by state-licensed sportsbooks are also swaps. Since state-licensed sportsbooks are not DCMs and deal with non-ECP customers, these transactions may violate federal law, creating a situation where the CEA’s field preemption could render state-authorized sports gambling potentially illegal.

Issue #3 - Contradiction of Congressional Intent: The CFTC’s regulatory openness to these products contradicts the legislative record of the Dodd-Frank Act, which specifically placed “gaming” on a list of activities the CFTC was authorized to prohibit. Congress originally intended to bar event contracts that “exist predominantly to enable gambling”.

Issue #4 - Erosion of Definitional Integrity: The interpretation stretches the swap definition, which historically requires a bilateral, executory exchange of a series of payments over time, to include a prediction contract, which is a single, binary, terminal payout. This structural mismatch sacrifices definitional integrity for the sake of regulatory expansion.

Let’s turn this into a table and compare Lothian’s views to ours.

You might observe: “You are mostly agreeing with him.”

We do! For the most part, it’s not his analysis that we take issue with. It’s the moment he re-evaluates his premise when he sees the conclusions; it’s akin to denying that it rained just because we didn’t like getting wet. We must evaluate the existence of rain based on standalone reasoning, not the outcome.

To do that, we need to separate three concepts that are often blended together–sometimes consciously, sometimes not.

The 3P-Framework: Preemption, Permissibility, Parallelism

We’ve discussed this in many places. This podcast is a great place to start:

The key insight: Prediction markets give us a three-in-one special. Three legal questions, all of which must be resolved:1

Question 1 - Is sports a commodity/are sport event contracts swaps?

(federal jurisdiction)Question 2 - Are sports event contracts permissible?

(gaming/economic purpose)Question 3 - Can there be an overlap between federal and state powers?

(off-exchange futures trading)

We aren’t the only ones who see this. Here’s Andrew Ross Sorkin chatting with Michael Selig on CNBC–touching on all three:

ARS’s first statement:

This is a federal issue vs. a state rights issue. That’s what this seems to be about.

That’s the preemption part of it. Not all of it, but the right starting point.

Then ARS observes:

But Mike, you do recognize… For a very long time… there were remarkable debates… about whether there should be sports betting. Whether it should be allowed.

That’s the permissibility part.

A few minutes later he asks:

There’s a question about, if you’re a state, whether you should have any say… at all?

That’s the parallelism part. Now the trio is complete.

Within five minutes, Andrew Ross Sorkin got to the bottom of the issue. That’s what smart journalists do.

The problem? The courts are not dealing with all three questions. They’re not even dealing with two. They are still at the preemption stage, and their hands are full with over 50 lawsuits.

To understand why, you may want to engage with the concept of litigation sequencing:

Lothian’s Framework, Re-Delineated

Lothian actually touches all three questions. He isn’t missing a key issue. He simply doesn’t delineate them cleanly, and that lack of separation drives him to the wrong conclusion. Once we separate the strands, the outcome changes dramatically.

The Retail Trader Violation

We haven’t talked much about this, but we’re in full agreement. If sports event contracts are swaps (and we believe they are), that’s where the law takes you.

This is a preemption and parallelism issue.

The Sportsbook Illegality

We’ve discussed this extensively. One example:

Again, in full agreement with Lothian. If sports event contracts are swaps (and we believe they are), that’s where the law takes you.

This is a preemption and parallelism issue.

Contradiction of Congressional Intent

This is where things get interesting. We agree that Congress did not intend the CFTC to regulate sports event contracts. But what we’re observing today is not a result of these contracts being swaps. It’s the result of the CFTC treating the “gaming” prong very differently than it did just a few years ago, when ErisX attempted the same thing (and theirs were arguably less intrusive because they proposed a self-imposed retail limit).

This is the key distinction. Lothian looks at this and says:

Congress couldn’t have intended a nationalized sports gambling scheme,

so these can’t be swaps.

We look at it and say:

Congress couldn’t have intended a nationalized sports gambling scheme, so the CFTC is ignoring the statute (and its own regulations). That’s an APA issue.

The CFTC’s refusal to review Kalshi contracts, and more broadly, its general stance, actions, statements, non-actions and silence regarding sports event contracts, are themselves reviewable agency actions (or failures to act) under the Administrative Procedure Act. Congress did not mandate that the CFTC review every contract, but it certainly expected the agency to conduct a review when the contracts at issue may involve gaming, and the legislative record makes clear that Congress felt strongly about that obligation:

In fact, the CFTC itself took its discretionary authority one step further and wrote Reg. 40.11(a), a prohibition clause; one it completely ignores today.

If Lothian looks at this picture and finds it impossible to reconcile, we agree. But the solution is not to interpret the statute in a way that denies the CFTC exclusive jurisdiction Congress granted to the Commission. The much better solution is acknowledging the fact that the regulator is simply acting inconsistent with congressional intent, and the legal mechanism that closes that gap is the APA.

Erosion of Definitional Integrity

Lothian dislikes that the swap definition has expanded to cover binary-outcome contracts. A couple quick points:

That’s what Congress ordered.

This shift predates Dodd-Frank. The real expansion happened in 2000 with the CFMA:

What Lothian really dislikes is not the expanded definition, but the fact that the CFTC is turning away from what Congress strongly expected them to do. That’s not a definition or preemption problem.

That’s a permissibility problem.

Lothian posted a recap, summarizing his prediction-market pieces. How he described the one we’re analyzing proves the point:

I walk through how the Commodity Exchange Act’s broad swap definition can technically catch these contracts, but I maintain that treating them as swaps obscures the crucial distinction between risk‑transfer instruments and gambling‑style wagers.

Yes, the definition catches these contracts. Treating them as swaps isn’t the problem. Treating them as permissible swaps is.

And by adding just that one word, the conclusion turns upside down. Prediction markets can’t offer these contracts–not because they aren’t swaps–but because they aren’t permissible swaps. And because of how Congress revised the CEA through Dodd-Frank, state-regulated sportsbooks cannot offer them either.

Prediction markets are top-of-mind for many people these days, including myself.

What’s different for me is that I started thinking about these issues long before prediction markets entered public consciousness. Before Kalshi and before Polymarket. Before ErisX and before Murphy.

How? How did I become that person?

It’s a long story, but the time has come to share it. Next up: How and why I wrote a 2013 Supreme Court petition. The question I asked:

Is sports performance an excluded commodity under the Commodity Exchange Act?

We didn’t discuss it in this particular post, but the Wire Act is also implicated as part of the second inquiry (permissibility).